This story requires a subscription

This includes a single user license.

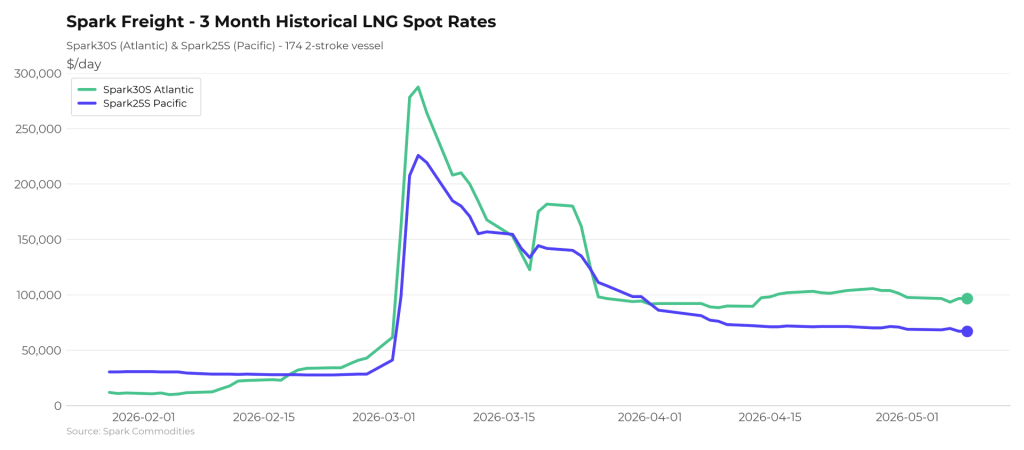

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) rates dropped $1,000 to $96,500 per day this week compared to the week before.

Afghan said Spark25S (Pacific) rates dropped $1,750 to $67,000 per day.

“Strange situation”

“The dormant spot market East of Suez has been somewhat roused this week by a number of requirements firming up for late May through mid-June. Qalhat liftings continue to feature heavily, with wide disparities in additional war risk premia playing a key role in assessment of candidates. Uncertainty on production across various load terminals in Australia as well as Canada continues to stall prompt transactions and stifle liquidity,” Fearnley LNG said in its weekly LNG report on Thursday.

“The West is now enjoying a far more active spot market and is continuing to command a premium on freight rates for the May-June fixing window. This comes despite recent disruptions at Freeport LNG leading to several canceled cargoes, and subsequent unexpected short-term length from scheduled lifters. Although open tonnage feels a little sparse, firm requirements have seen interest from 2-stroke owners but not with sufficient competition to force rates significantly lower, while a preference for worldwide redelivery optionality is supporting the price floor,” the Oslo-based advisory and brokering firm said.

Fearnley LNG said that “a rush of activity from the portfolio players resulted in a flurry of term fixtures late last week, as charterers sought coverage into Q1 2027.”

“Modern 2-strokes with worldwide redelivery are the vessels of choice, owing to charterers’ need for maximum geographical optionality as a hedge against a bullish LNG price outlook. A widening arbitrage and the highest levels of inter-basin cargoes in over a year, coupled with low EU storage levels and injections down 20 percent on last year, is signaling strong East-West jostling for volumes and subsequent LNG price volatility. We’re now in the strange situation where forward 2-stroke availability is tightening while we experience fleet oversupply on the spot,” it said.

Reduced demand for delivery slots in Northwestern Europe

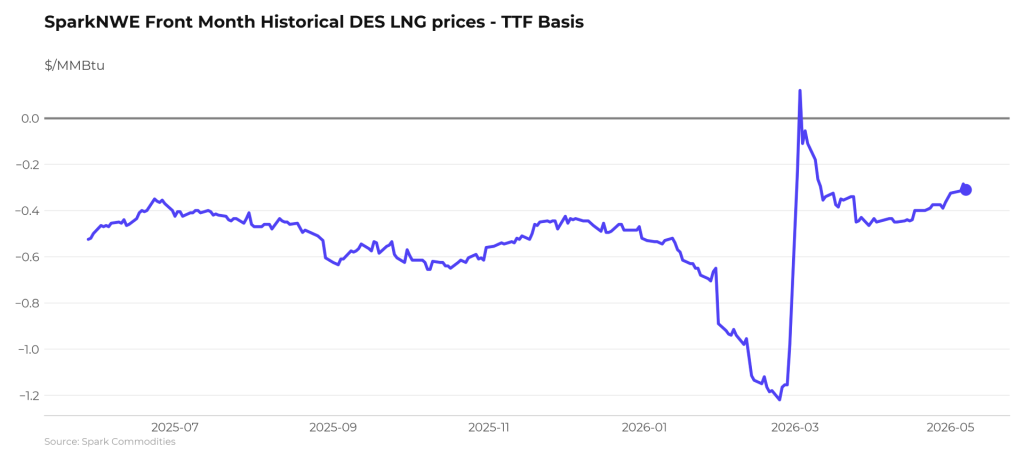

In Europe, the SparkNWE DES LNG dropped compared to last week.

“The SparkNWE front-month DES LNG price for June delivery is assessed at TTF-$0.310, indicating continued reduced demand for delivery slots into NW-Europe. The outright NWE DES LNG price is now at $14.725/MMBtu, dropping $1.058 since Tuesday,” Afghan said.

“The US prompt (M+1) arb to Asia via COGH is currently open and priced at +$0.229/MMBtu – this marks a week-long strengthening signal for US prompt cargoes to deliver to Asia instead of Europe,” he said.

Afghan added that “the US M+1 arb via Panama remains open and firmly pointing to Asia for the 10th week running, now priced at +$0.901/MMBtu – the strongest signal to Asia via the canal since mid-March.”

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU rose from last week and were 34.26 percent full on May 7, 2026.

Gas storages were 32.49 percent full on April 30, 2026, and 41.58 percent full on May 7, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in June 2026 settled at $16.840/MMBtu on Thursday.

Last week, JKM for June settled at 16.865/MMBtu on Friday, May 1,

Front-month JKM remained flat on Monday. It rose to 17.035/MMBtu on Tuesday and dropped to 16.850/MMBtu on Wednesday.