This story requires a subscription

This includes a single user license.

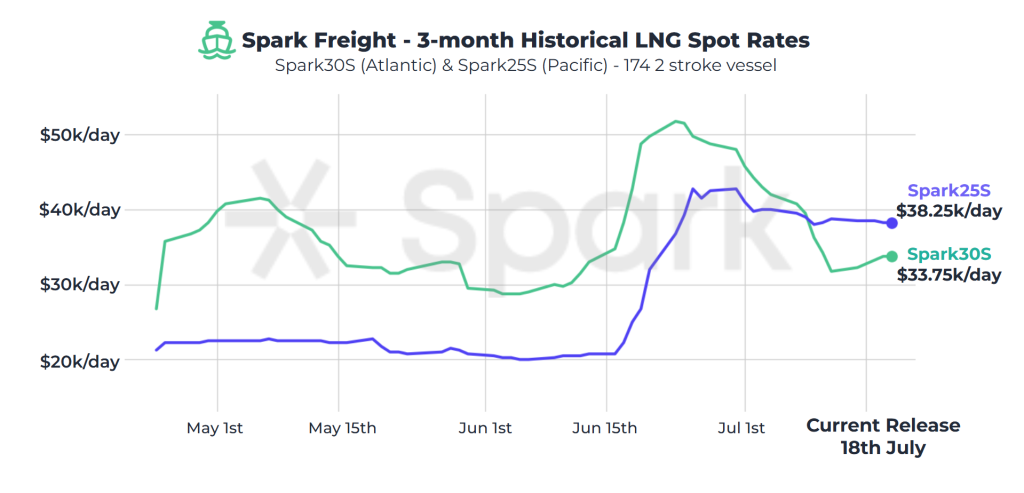

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) freight rates increased by $2,000 to $33,750 per day.

Meanwhile, Spark25S (Pacific) rates stayed relatively steady at $38,250 per day and continued to price at a premium to Atlantic rates, he said.

European prices down

In Europe, the SparkNWE DES LNG dropped compared to last week.

“The SparkNWE DES LNG front month price for August decreased by $0.370, pricing in at $11.269/MMBtu, whilst the basis to the TTF remains relatively steady at $0.415/MMBtu,” Afghan said.

He said the “US front-month arb to NE-Asia (via the Cape of Good Hope) closed out further by $0.094, pricing in at -$0.251/MMBtu – this is the lowest US front-month arb assessment in over three months, and continues to incentivise US cargoes to deliver to Europe.”

“The US front-month arb to NE-Asia via Panama closed out for the first time in seven weeks, now assessed at -$0.053/MMBtu and also pointing to Europe instead of Asia,” Afghan said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU continued to rise and were 63.88 percent full on July 16.

Gas storages were 61.95 percent full on July 9, and 81.59 percent full on July 16, 2024.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in September 2025 settled at $12.180/MMBtu on Thursday.

Last week, JKM for August settled at 13.115/MMBtu on Thursday, July 11.

Front-month JKM remained the same on Monday. It dropped to 13.105/MMBtu on Tuesday and to $12.405 on Wednesday.

State-run Japan Organization for Metals and Energy Security (Jogmec) said in a report earlier this week that JKM for last week “rose to high-$12s/MMBtu on July 11 from mid-$12s/MMBtu the previous weekend.”

“JKM rose to high-$12s/MMBtu due to increased demand from rising temperatures in Northeast Asia and remained at that level due to a limited availability of cargoes arriving in August,” it said.

Asia’s LNG physical market

The Platts Market on Close assessment process for Asia’s LNG physical market during the August pricing period recorded a sharp 86.43 percent increase year-over-year, but fell 20.76 percent month-over-month as the market contended with geopolitical uncertainty and the seasonal summer demand peak.

According to a report by Platts, part of S&P Global Commodity Insights, a total of 334 bids, 128 offers, and 19 trades were recorded for deliveries across H2 July, August, and September, involving 23 entities.

The majority of market activity centred around deliveries into the Japan-Korea-Taiwan-China region. In addition, three bids for deliveries into China, one bid for Japan, one offer for Thailand, and two offers for the broader JKT region were reported, the report said.

The 19 trades, amounting to approximately 1.24 million mt of LNG, saw Glencore emerge as the most active buyer, securing nine cargoes, followed by Vitol with seven. BP, TotalEnergies, and Uniper each purchased one cargo, Platts said.

On the sell side, PetroChina led with five cargoes, followed by Vitol with three, and BP and Shell with two each. Osaka Gas, QatarEnergy Trading, TotalEnergies, Unipec, Socar, Chevron, and CNOOC each sold one cargo, Platts noted.