This story requires a subscription

This includes a single user license.

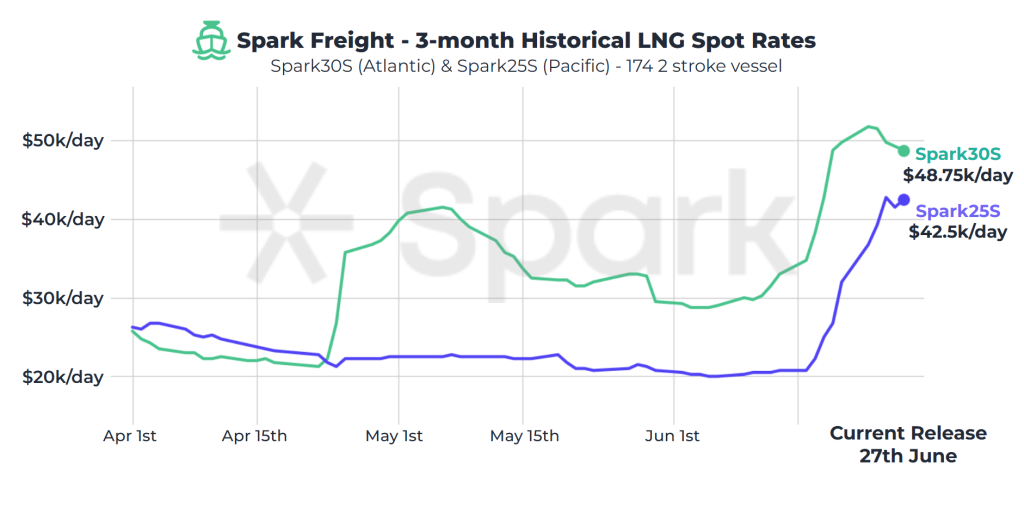

“Spark30S (Atlantic) freight rates remained relatively steady this week, dropping by $1,000 to $48,750 per day this week,” Spark’s data lead Qasim Afghan told LNG Prime on Friday.

In comparison, Spark25S (Pacific) rates continue to rise, increasing by $10,500 to $42,500 per day, as tight vessel availability continues to affect the market, he said.

European prices dip

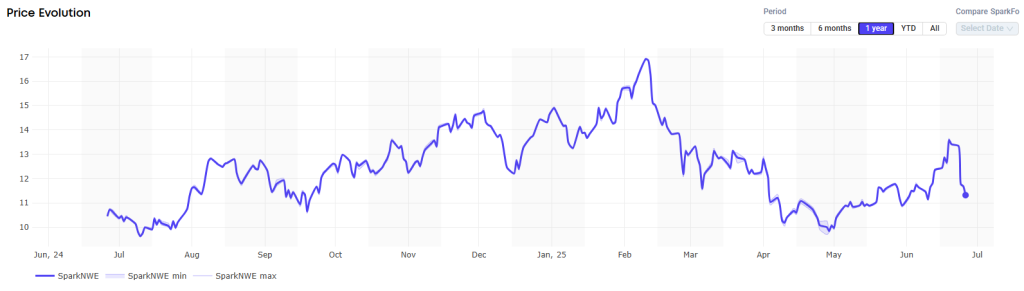

In Europe, the SparkNWE DES LNG dipped compared to last week.

“The SparkNWE DES LNG front month price for July fell by $2.267 to $11.320/MMBtu, the largest week-on-week drop in DES LNG prices since December 2022 as TTF prices fell in response to the ceasefire announcement in the Middle East,” Afghan said.

He said the basis to the TTF continued to narrow for the eighth consecutive week, assessed at $0.355/MMBtu and indicating reduced demand for LNG delivery slots in NW-Europe.

“The US front-month arb to NE-Asia (via the Cape of Good Hope) opened up for the first time in two months in response to TTF prices sharply falling. However, since then, the arb has closed out again and is now marginally pointing to Europe, pricing in at -$0.039/MMBtu,” Afghan said.

“The US front-month arb to NE-Asia via Panama continues to point to Asia for a fourth week running, assessed at $0.264/MMBtu,” he said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU continued to rise and were 57.15 percent full on June 25.

Gas storages 54.69 percent full on June 18, and 75.97 percent full on June 25, 2024.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in August 2025 settled at $13.325/MMBtu on Thursday.

Last week, JKM for August settled at 14.255/MMBtu on Friday, June 20.

Front-month JKM rose to 14.460/MMBtu on Monday. It dropped to 13.520/MMBtu on Tuesday and rose to 13.540/MMBtu on Wednesday.

State-run Japan Organization for Metals and Energy Security (Jogmec) said in a report earlier this week that JKM for last week “rose to high-$14s/MMBtu on June 20 from mid-$13s/MMBtu the previous weekend.”

“JKM had been rising for six consecutive business days due to rising geopolitical tensions in the Middle East, and although it temporarily declined on June 19, it rebounded on June 20 amid recurrence of supply concerns. Despite record-setting heat across Japan, end-user‘s demand remained relatively stable, and spot procurement activity continued to be limited,” Jogmec said.