This story requires a subscription

This includes a single user license.

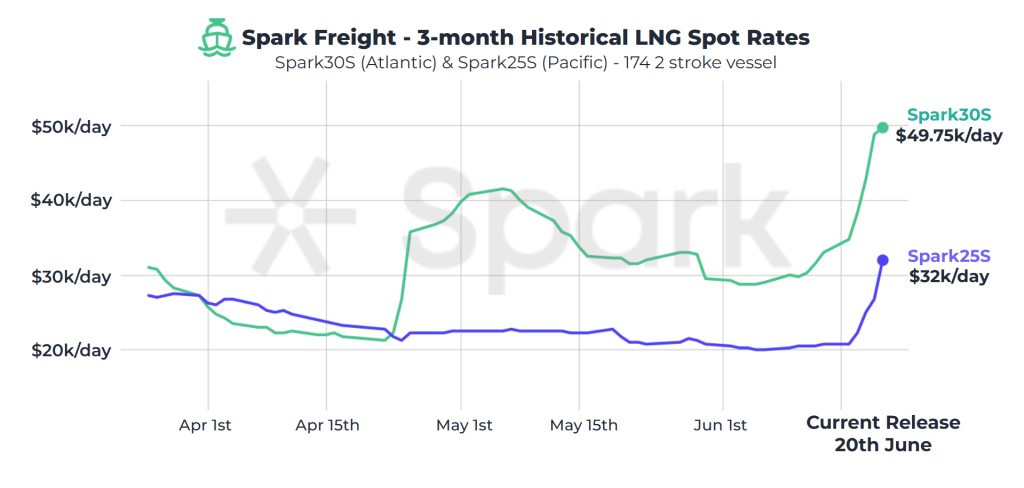

“Spark30S (Atlantic) freight rates continue to rise for a second consecutive week, increasing by $16,750 to $49,750 per day this week – the largest week-on-week increase in Atlantic rates since October 2023,” Spark’s data lead Qasim Afghan told LNG Prime on Friday.

Meanwhile, Spark25S (Pacific) rates, which have remained relatively steady for over two months, rose by $11,250 to $32,000 per day.

“This rise in global LNG freight rates has been largely due to tight vessel availability, partially caused by the US arb becoming increasingly marginal and no longer strongly pointing to Europe, as well as market sentiment around the geopolitical tension in the Middle East,” Afghan said.

Both Atlantic and Pacific freight rates are now at their highest levels since October last year, he said.

European prices surge

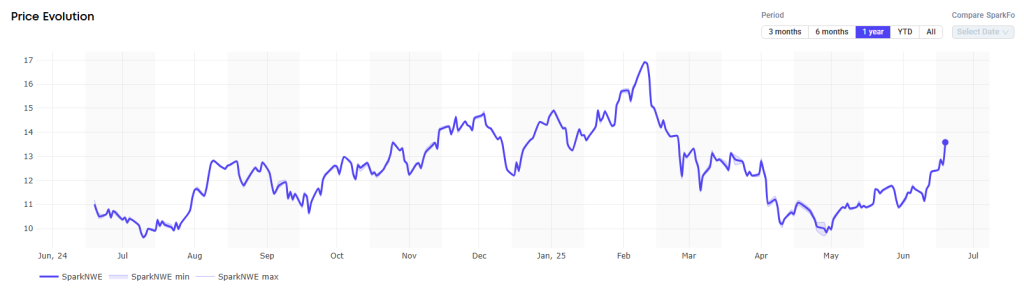

In Europe, the SparkNWE DES LNG rose compared to last week.

“The SparkNWE DES LNG front month price for July increased by $1.772 to $13.587/MMBtu, marking an almost 15 percent w-o-w increase as the TTF rose in response to events in the Middle East,” Afghan said.

He said the basis to the TTF continued to narrow for the seventh consecutive week, assessed at $0.405/MMBtu and indicating reduced demand for LNG delivery slots in NW-Europe.

“The US front-month arb to NE-Asia (via the Cape of Good Hope) reached breakeven levels on Monday as the increase in JKM prices outpaced the TTF in response to the escalating events in the Middle East. However, since then, the arb has closed out again and is now more strongly pointing to Europe, pricing in at -$0.114/MMBtu,” Afghan said.

“The US front-month arb to NE-Asia via Panama continues to point to Asia for a third week running, assessed at $0.261/MMBtu,” he said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU continued to rise and were 54.69 percent full on June 18.

Gas storages were 52.44 percent full on June 11, and 74.09 percent full on June 18, 2024.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in August 2025 settled at $13.880/MMBtu on Wednesday.

Last week, JKM for July settled at 12.504/MMBtu on Friday, June 13.

Front-month JKM rose to 13.585/MMBtu on Monday and to 14.005/MMBtu on Tuesday.

State-run Japan Organization for Metals and Energy Security (Jogmec) said in a report earlier this week that JKM for last week “rose to mid-$13s/MMBtu on June 13 from high-$12s/MMBtu the previous weekend.”

“JKM fell to low-$12s/MMBtu in the first half of the week due to weak demand in Asia, but rose to high-$12s/MMBtu on June 12 due to rising summer demand. It then soared to mid-$13s/MMBtu on June 13 due to rising geopolitical tensions following Israel’s attack on Iran,” Jogmec said.

Israel-Iran

Several reports said this week that QatarEnergy has instructed masters of LNG carriers to remain outside the Strait of Hormuz and to enter the Gulf only the day before loading, amid military strikes between Israel and Iran.

Tensions around Hormuz have led to disrupted LNG shipping patterns, with Kpler identifying at least seven LNG tankers behaving unusually in the area.

As geopolitical instability intensifies, shipping operators are exercising increased caution, Kpler said in a report.

“The Strait of Hormuz, which channels a fifth of the world’s LNG, is once again proving vulnerable to regional tensions and suspected signal interference,” it said.