This story requires a subscription

This includes a single user license.

Cheniere is the largest LNG exporter in the US.

The company’s Sabine Pass facility in Louisiana currently has a capacity of about 30 mtpa following the launch of the sixth train in February 2022, and its three-train Corpus Christi plant in Texas can produce about 15 mtpa of LNG.

The Corpus Christi facility is undergoing expansion to add more than 10 mtpa of capacity, while the company also plans further expansion for this plant and the Sabine Pass plant.

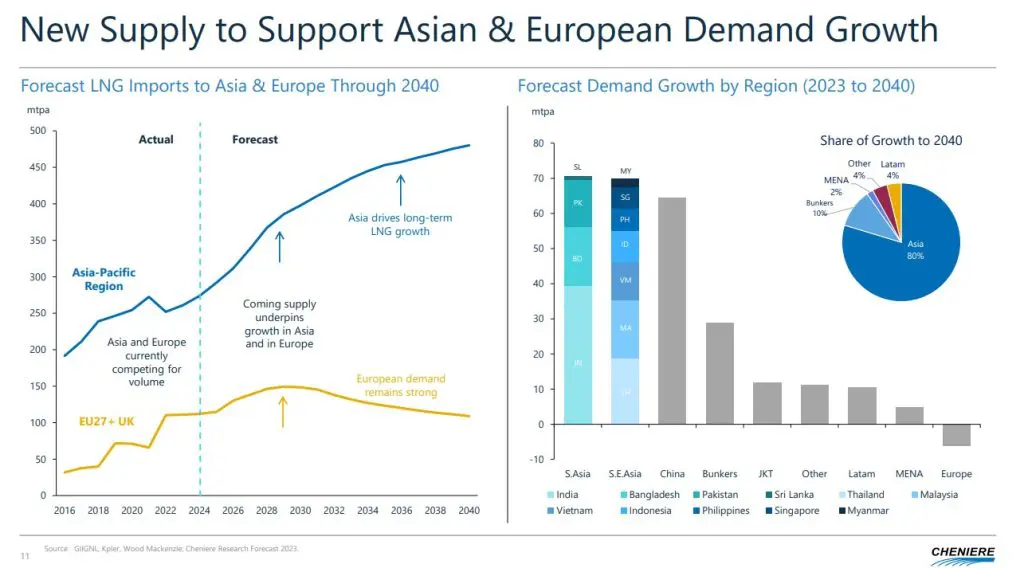

Asia and Europe

Cheniere produced and exported about 3,570 cargoes from its Sabine Pass and Corpus Christi terminals since 2016.

During the last couple of years, most of these cargoes landed in Europe.

However, after nearly two full years of focus on Europe and its energy crisis, Asia has in the first half of 2024 regained the spotlight in the LNG marketplace, Cheniere’s executive VP and chief commercial officer, Anatol Feygin, said during the second-quarter conference call on August 9.

“We believe this rebound is supportive of our long-term market thesis, namely that as the supply curve pushes out into the right and market liquidity continues to increase in the coming years, we will see incremental demand growth in both Europe and Asia,” he said.

Feygin said market analysts agree that Asia remains the primary driver of LNG demand growth over the longer term.

“As you can see from the chart to the left, we expect Asian demand to nearly double by 2040. So the supply availability is not constrained,” Feygin said.

“However, Europe will still need significant volumes of LNG now and in the long-term and will continue to compete with Asia as domestic production and regional pipe imports continue to decline,” he said.

China is not the only growth driver

He said the growth in Asia is not driven by China alone, but rather spread across numerous markets in Asia, enhancing the durability of growth in the region over the coming decades.

“On previous calls, we have highlighted the significant growth potential of South and Southeast Asian markets and believe that these stands to particularly benefit from the coming increase in LNG supply, supporting grid stability and ensuring system flexibility and resiliency,” Feygin said.

Ahead of this supply cycle, Cheniere expects the market to continue to balance primarily on the demand side.

The expectation of growing supply from 2026 onwards should alleviate the constraints on demand growth, especially as moderate prompt LNG and gas prices prevail, he said.

“This would help both Europe and Asia, equally, in realizing security of supply as Europe will be better able to meet its requirements to replace Russian gas while backstopping growth in renewables, and Asia will be better equipped to displace coal and offset regional production declines while underpinning investments in gas infrastructure and high-growth developing economies,” Feygin said.

Cheniere’s 40th delivery market

Talking about the second quarter this year, he said the supply-demand balance remained “delicate” in the LNG market.

“Looking at the center charts, global LNG trade growth was constrained by minimal supply growth during the quarter, with Asia’s increased demand met by attracting cargoes in the Atlantic Basin via higher prices,” he said.

Feygin said this demand pull from Asia is further evidenced by US LNG export flows, which continue to shift from Europe to Asia during the quarter.

“The growth in global supply was partially offset as Egypt flips back to an LNG importer and other export facilities suffered protracted outages,” he said.

“The limited incremental supply, Asia’s consumption growth was primarily dominated by China and India, leaving little volume for relatively new market areas such as Hong Kong, Vietnam, and the Philippines, which actually became our 40th delivery market last week,” he said.

“We expect this seemingly fragile market balance to continue until additional LNG export capacity comes online,” he said.