This story requires a subscription

This includes a single user license.

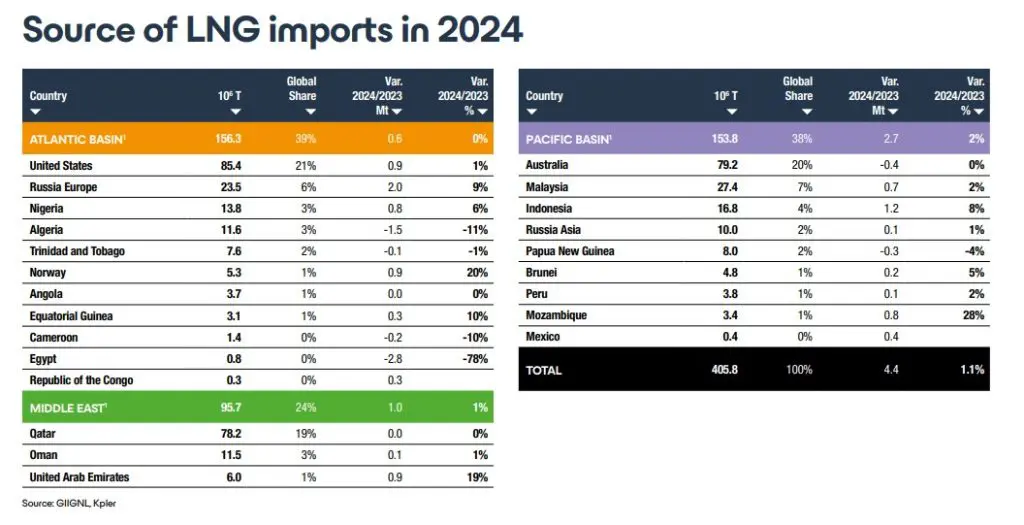

GIIGNL’s previous report showed that global LNG imports rose 2.1 percent in 2023 to 401 million tons.

The Paris-based group said in the new report that global LNG trade “remains remarkably steady, despite starkly contrasting regional dynamics.”

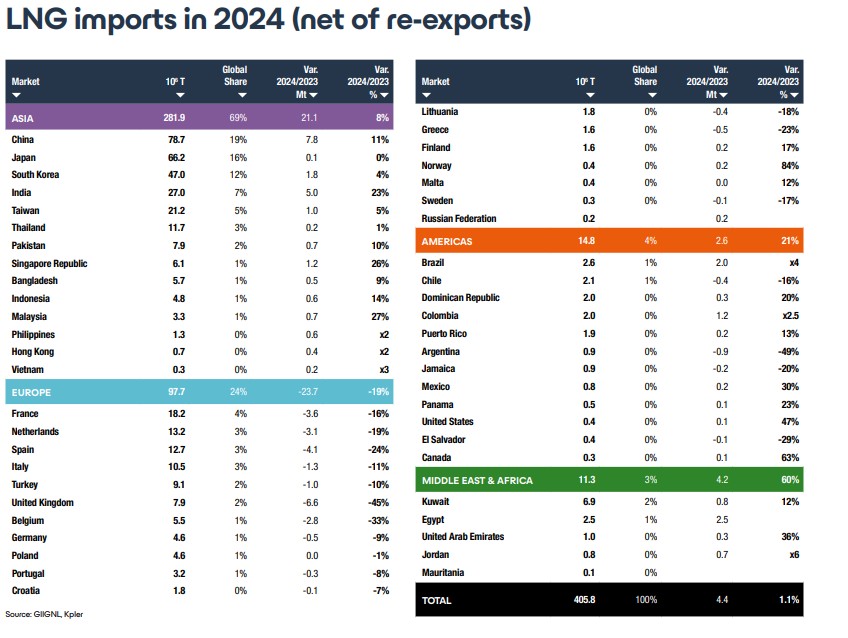

GIIGNL said Asia continued its healthy expansion, propelled by rising demand in China and India, while Europe experienced its largest-ever slump in LNG imports amid declining gas consumption.

However, the vigorous growth observed in Asia, along with strong performances in the Middle East and Americas, helped offset Europe’s downturn, keeping global LNG trade nearly flat.

Overall, global LNG volumes grew by a modest 1 percent, with the number of importers totaling 49 and exporting countries expanding to 22, as Mexico and the Republic of the Congo entered the market, GIIGNL said.

In Asia, LNG imports surged across nearly all markets, with China spearheading the growth.

China’s robust increase in LNG imports was driven by the steady expansion of industrial production, heightened gas demand for power generation, and growing LNG consumption in the trucking sector, GIIGNL said.

Liquefaction capacity reached 492 MTPA

GIIGNL said global liquefaction capacity reached 492 MTPA in 2024, including 14 MTPA of floating liquefaction units (FLNG).

Three new projects for a total of 8.6 MTPA of liquefaction capacity started in 2024, including two FLNG accounting for 2 MTPA.

The new projects are 0.6 MTPA Congo FLNG in the Republic of Congo, 6.6 MTPA Arctic LNG 2 in Russia, and 1.4 MTPA Altamira Fast LNG in Mexico.

In addition, two debottleneck projects were completed in 2024 for a total of 1.9 MTPA: 1.5 MTPA at Freeport LNG and 0.4 MTPA at Ichthys.

FIDs were taken on four liquefaction projects in 2024, with a total capacity of around 14 MTPA: 1 MTPA Marsa LNG in Oman, 9.6 MTPA Ruwais LNG in the UAE, 3.3 MTPA Cedar LNG in Canada and a 1.2 MTPA FLNG project in Indonesia.

Regas capacity

GIIGNL said global regasification capacity reached 1188 MTPA as of end of 2024, following the addition of 31 MTPA from 12 new terminals commissioned in 2024 and 19.5 MTPA from 7 completed expansion projects.

Asia continues to lead the capacity growth, especially China with 29 MTPA of incremental capacity. Europe and South America opted for floating-based LNG solutions.

Three floating terminals started operations in Europe (2 in Germany and 1 in Greece) adding 14 MTPA of regasification capacity to reinforce the European security of supply.

Also, three FSRU-based LNG terminals were commissioned in Brazil for a total of 13.5 MTPA.

831 vessels

GIIGNL said the total LNG tanker fleet consisted of 831 vessels at the end of 2024.

It included 52 FSRUs and 79 vessels (53 LNGBVs + 26 small-scale LNG carriers) of equal or less than 30,000 cubic meters.

Total cargo capacity at the end of 2024 stood at 124 million cubic meters.

Moreover, total operational capacity (vessels known to be in service) amounted to 122 million cubic meters.

In 2024, the average spot charter rate for a 160,000 cubic meters TFDE LNG carrier stood at around $42,200/ day, compared to an average of around $97,100/day in 2023.

GIIGNL said that a total of 67 vessels were delivered in 2024, compared to 41 vessels in 2023.

The group said that the number of new orders reached a total of 89 units, compared to 66 new orders in 2023.

At the end of 2024, the orderbook consisted of 348 units (60.5 million cubic meters), including 4 FSRUs and 18 LNGBVs.

The orderbook represented 49 percent of existing fleet capacity.

GIIGNL said that 103 units on order were scheduled for delivery in 2025.