This story requires a subscription

This includes a single user license.

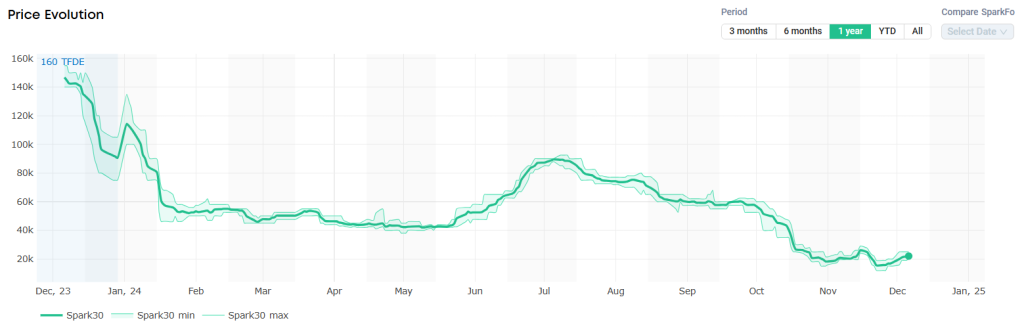

Last week, Atlantic LNG shipping rates remained below $20,000 per day.

“November finished pricing in last week at $19,700 – this is the lowest priced month on record for Spark30S (Atlantic) freight rates for a 174 2 stroke vessel,” Qasim Afghan, Spark’s commercial analyst, told LNG Prime on Friday.

“This week, Spark30S rates rose for a second consecutive week, increasing by $4,500 to $22,000 per day, whilst Spark25S Pacific rates stayed relatively steady this week, falling by $250 to $23,750 per day,” Afghan said.

Spot LNG charter rates are expected to remain weak in the upcoming weeks mainly due to a large number of newbuilds entering the market.

European prices climb

In Europe, the SparkNWE DES LNG rose compared to $14.083/MMBtu last week.

“The SparkNWE DES LNG front month price for January delivery is assessed at $14.20/MMBtu – this is over $0.50 lower than the start of this week, when SparkNWE prices reached a year-high of $14.777/MMBtu,” Afghan said.

He said the discount to the TTF kept steady this week at -$0.225/MMBtu.

“The US arb to NE-Asia (via the Cape of Good Hope) for January is currently firmly closed, pricing in at -$0.467/MMBtu and signaling that US cargoes are incentivized to deliver to NW-Europe instead,” Afghan said.

“With the Panama LoTSA slot allocation due to start in January, the Panama Canal is set to become a feasible option again for LNG vessels in 2025. However, the US arb to NE-Asia via Panama Canal is currently also signaling US cargoes to NW-Europe, albeit it much more marginally, pricing in as closed at -$0.231/MMBtu and remaining closed until Nov25,” he said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU continued to decline and were 83.61 percent full on December 4 .

Gas storages were 86.65 percent full on November 27 and 93.17 percent full on December 4, 2023.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in January 2025 settled at $15.065/MMBtu on Thursday.

Last week, JKM for January settled at 14.925/MMBtu on Friday, November 22.

Front-month JKM rose to 15.115/MMBtu on Monday and 15.125/MMBtu on Tuesday. It dropped to 15.075/MMBtu on Wednesday.

State-run Japan Organization for Metals and Energy Security (JOGMEC) said in a report earlier this week that JKM for last week (November 25– November 29) fell to high-$14s on November 29 from mid-$15s the previous weekend.

“JKM rose significantly last week, but this week continued sluggish demand and high inventory led to a downward trend throughout the week,” JOGMEC said.

Chinese LNG companies selling Jan-Feb 2025 cargoes

S&P Global Commodity Insights said on Friday, citing market participants, that some Chinese state-owned and second-tier oil and gas companies have been looking to sell LNG cargoes for the January-February 2025 period to alleviate pressure from growing inventory and weak domestic demand.

According to the report, the selling interest reflects expectations that regional heating demand is unlikely to surge as winter progresses, which would help lower spot Asian LNG prices, despite some demand for spot cargoes from Europe that would typically trigger price competition and tighten supply.

Opportunistic Chinese LNG importers have previously sold LNG purchased under relatively cheaper oil-indexed contracts at higher spot prices.

Platts assessed JKM for January at $14.983/MMBtu on December 5, while oil-indexed LNG is likely to cost around $11-$12/MMBtu, based on current oil prices of around $75/b, the report said.