This story requires a subscription

This includes a single user license.

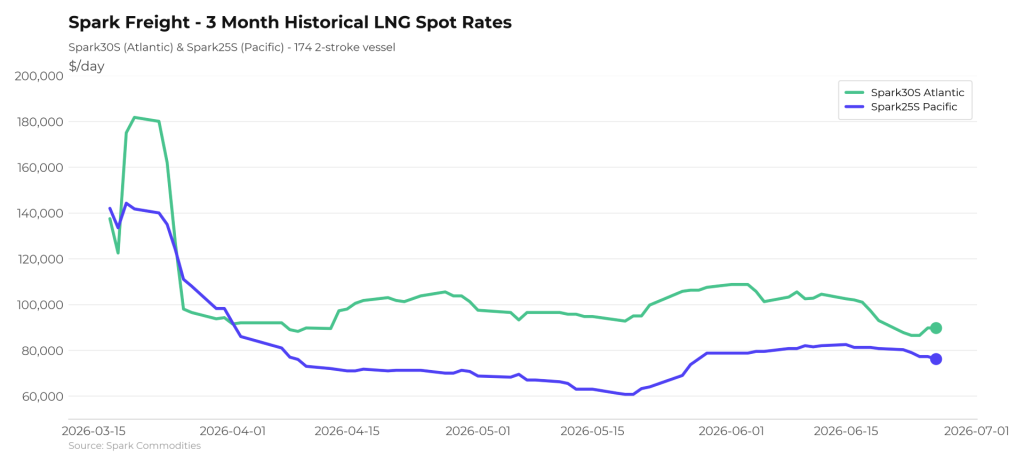

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) rates remained relatively steady this week, dropping $3,250 week-on-week to $89,750 per day.

Similarly, Spark25S (Pacific) rates have dropped $4,500 to $76,250 per day, he said.

Ras Laffan loadings

“Although the status of the Strait of Hormuz remains unclear, there are encouraging signs from within the Gulf itself. This week, several QELM ships have transited the Strait and positioned themselves off Ras Laffan ahead of potential loadings,” Fearnley LNG said in its weekly LNG report on Thursday.

“As mentioned in our weekly digest, QatarEnergy have indicated output could ramp to approximately 50 percent (39 mtpa) within one month and approximately 80 percent (39 mtpa) within two months of safe passage resuming,” the Oslo-based advisory and brokering firm said.

According to Fearnley LNG, the disruption has “given a new lease of life to steamships, as their lower H&M insurance and subsequent AWRP make them a favorable choice for early transits through the Strait.”

“The spot market East of Suez remains subdued, with the few requirements being worked seeing multiple competing offers, and rates threatening to tick down accordingly. With JKM continuing to dip in reaction to the evolving news, charterers stand by to see if freight rates will follow,” Fearnley LNG said.

“Among US Gulf lifters, appetite for worldwide flex is waning, as the arb struggles to remain open. Intra‑Atlantic voyages to Europe are regaining their economic appeal and these shorter voyages may add some additional tonnage to the lists in the West. This is reflected in headline spot rates down from the Q2 peak earlier this month,” Fearnley LNG added.

European prices down

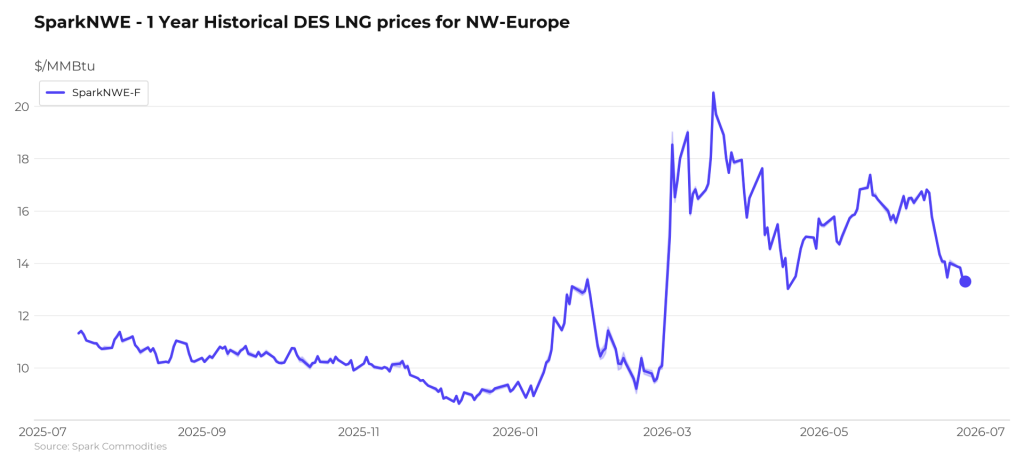

In Europe, the SparkNWE DES LNG rose dropped compared to last week.

“The SparkNWE front-month DES LNG price for July delivery is currently assessed at TTF-$0.170. The outright NWE DES LNG price is now at $13.302/MMBtu, decreasing $0.159 and marking the lowest front month DES LNG price for NW-Europe since mid-April,” Afghan said.

“Prompt US LNG cargo prices continue to drop, with the SparkUSG-Sabine FOB marker decreasing $0.116 week-on-week and priced at $12.089/MMBtu ($47.4M/cargo) as of yesterday’s close. US prompt cargoes are still valued $2.605 (+27 percent) higher than pre-war levels,” he said.

Moreover, Afghan said that “the US prompt (M+1) arb via COGH, having reached breakeven levels earlier in the week amidst uncertainty in the Iran ceasefire, remains closed and pointing to Europe, narrowing $0.149 week-on-week and currently priced at -$0.123/MMBtu.”

“The US M+1 arb via Panama remains open and firmly pointing to Asia, now priced at +$0.734/MMBtu – the arb signal to Asia via Panama has now persisted for 4 months, the longest consistent signal to Asia via Panama since 2024,” Afghan said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU rose from the previous week.

Gas storages were 47.43 percent full on June 25, 2026. The storages were 45.56 percent full on June 18, 2026, while the storages were 56.91 percent full on June 25, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in August 2026 settled at $15.385/MMBtu on Thursday.

Last week, JKM for August settled at 15.315/MMBtu on Thursday, June 18.

Front-month JKM rose to 15.860/MMBtu on Monday. It dropped to 15.740/MMBtu on Tuesday and 15.550/MMBtu on Wednesday.