This story requires a subscription

This includes a single user license.

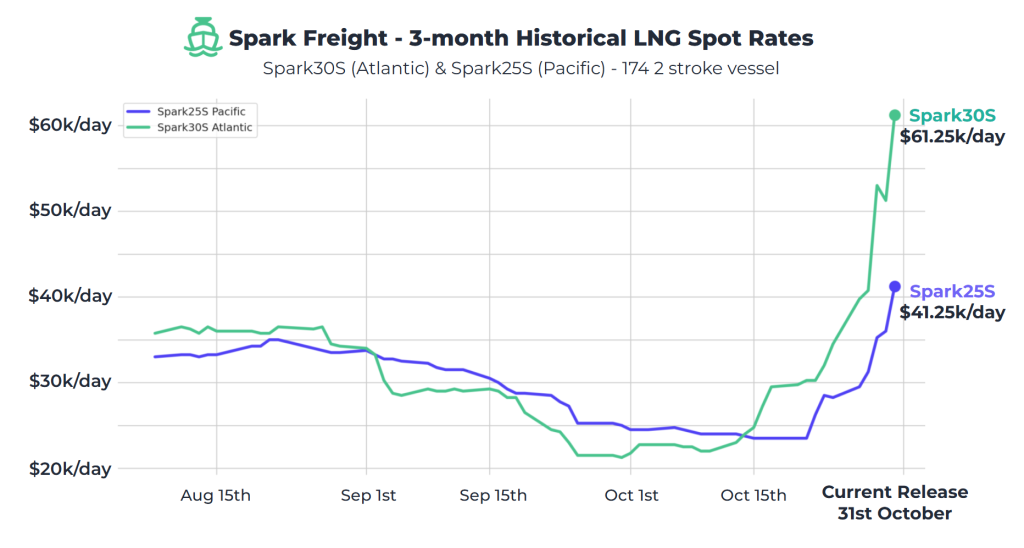

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) LNG freight rates have risen to a year-to-date high, increasing by $26,750 compared to the previous week.

Afghan said this is the largest week-on-week change since September 2023, and the highest Atlantic rate since September 2024.

Spark25S (Pacific) rates have also increased, rising by $13,000 to $41,250 per day.

“Recent FFA activity on Spark30 (Atlantic) has also increased the freight forward curve assessment for the remainder of Q4, with November rates increasing $28,000 w-o-w to $52,000 per day and December rates increasing $15,250 to $38,000 per day,” Afghan said.

“After months of flat market sentiment, the LNG shipping market has finally shown signs of momentum,” Fearnley LNG said in its weekly LNG report.

The Oslo-based advisory and brokering firm said rates across all three major regions have strengthened, led by gains in the Atlantic where levels have more than doubled in recent weeks.

“What started with discharge delays into Egypt and the knock-on impact on scheduling may have been the spark for the long-awaited winter rally that many thought wouldn’t come,” Fearnley LNG said.

“Asia is showing signs of renewed strength as cargo demand improves, pulling vessels off availability lists. East of Suez, 2-strokes are in short supply and TFDEs are now supporting firmer rates,” it said.

“Still, as history reminds us, a strong freight market can be fragile, and any cargo softening could reverse gains just as quickly,” Fearnley LNG said.

European prices down

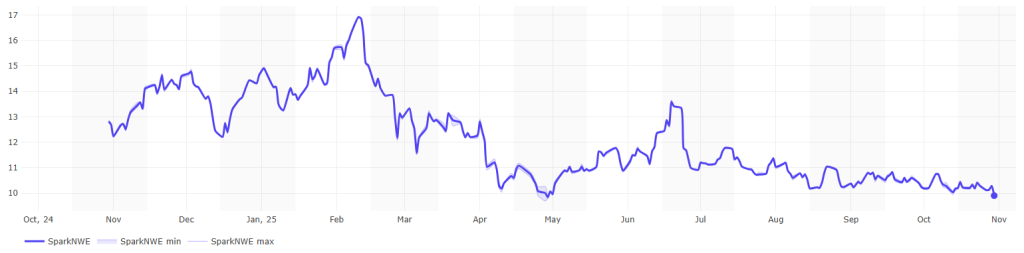

In Europe, the SparkNWE DES LNG dropped compared to last week.

“The SparkNWE DES LNG front month price for November dropped by $0.514 to $9.907/MMBtu this week, the lowest NW-Europe DES LNG price since July 2024,” Afghan said.

Moreover, the basis to the TTF “stayed relatively flat this week, assessed at -$0.615/MMBtu.”

“The US front-month arb (via the Cape) has once again closed and is now marginally pointing to Europe instead of Asia, with the latest price assessment at -$0.091/MMBtu,” Afghan said.

“The US front-month arb via Panama has remained open, pricing in at $0.127/MMBtu,” he said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU decreased slightly from last week and were 82.79 percent full on October 29, 2025.

Gas storages were 82.82 percent full on October 22, 2025, and 95.21 percent full on October 29, 2024.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in December 2025 settled at $11.130/MMBtu on Thursday.

Last week, JKM for December settled at 11.205/MMBtu on Friday, October 24.

Front-month JKM dropped to 11.120/MMBtu on Monday. It rose to 11.150/MMBtu on Tuesday and 11.215/MMBtu on Wednesday.

State-run Japan Organization for Metals and Energy Security (Jogmec) said in a report earlier this week that JKM for last week “fell to low-$11s/MMBtu on October 24 from mid-$11s/MMBtu the previous weekend.”

“JKM declined to high-$10s/MMBtu in the first half of the week as signs of winter demand remained weak across East Asia. The price then rose to mid-$11s/MMBtu toward the middle of the week on the back of accelerating temperature drops in the region but eased slightly to low-$11s/MMBtu on October 24 as some correction took place after the midweek rise,” Jogmec said.