This story requires a subscription

This includes a single user license.

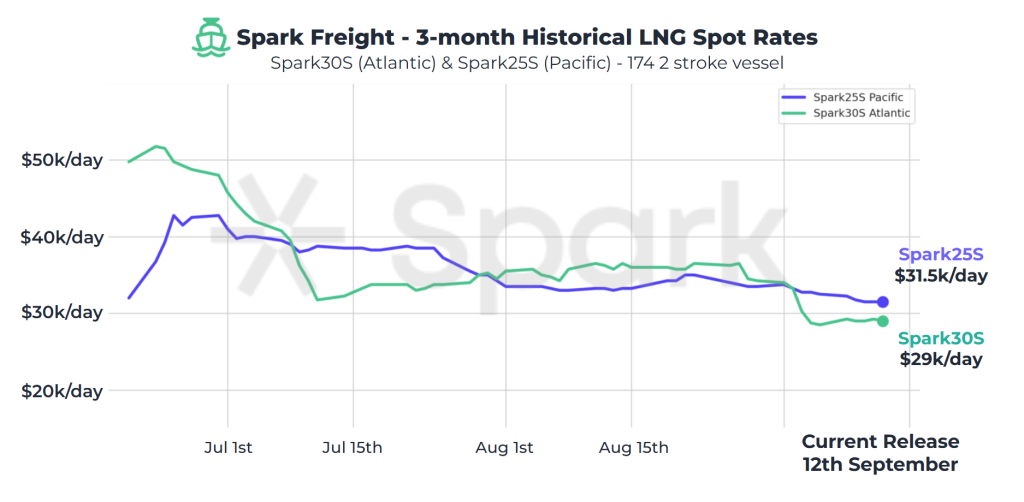

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) LNG freight rates “remained relatively steady this week $29,000 per day, whilst Spark25S (Pacific) fell a further $1,000 to $31,500 per day.”

“Spark’s Atlantic freight forward curve (Spark30FFA) prices for Winter 2025 are currently assessed at an average of $29,700 per day, with monthly rates remaining within an extremely tight range of $6,750 between now and March 2026,” he said.

European prices rise

In Europe, the SparkNWE DES LNG dropped compared to last week.

“The SparkNWE DES LNG front-month price for October increased by $0.103 to $10.545/MMBtu this week, whilst the basis to the TTF is narrowed to $0.565,” Afghan said.

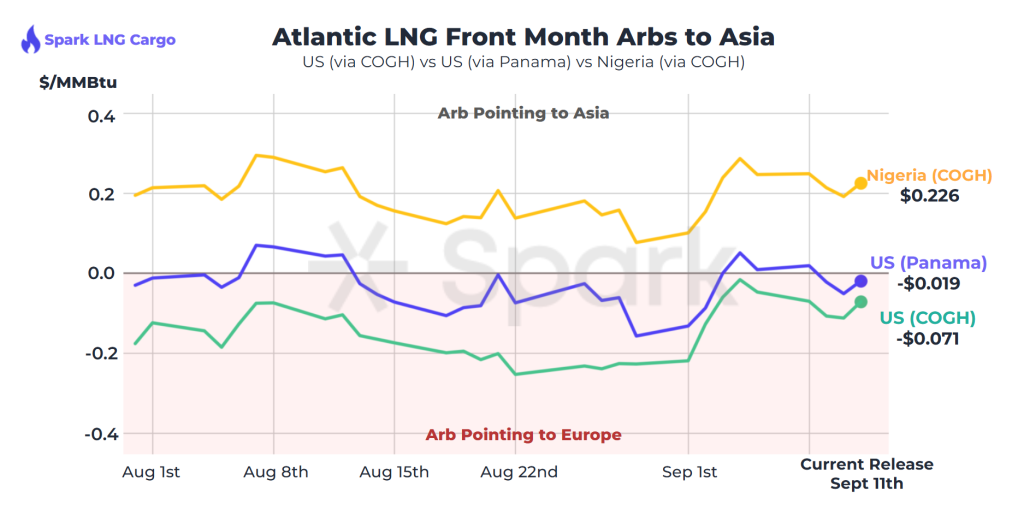

Moreover, “the US front month arb to NE-Asia (via the Cape of Good Hope) widened by $0.055 and now pricing in at -$0.071/MMBtu, still only marginally incentivising US cargoes to deliver to Europe,” Afghan said.

“The arb has now remained within a tight $0.31 range for the last five months, providing the longest, most stable arb signal for US cargoes in the last four years, indicating reduced volatility in the global LNG market. The US front-month arb to NE-Asia via Panama has closed out and is now assessed at -$0.019/MMBtu,” he said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU continued to rise and were 79.87 percent full on September 10.

Gas storages were 78.51 percent full on September 3, 2025, and 92.53 percent full on September 10, 2024.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in October 2025 settled at $11.345/MMBtu on Thursday.

Last week, JKM for October settled at 11.300/MMBtu on Friday, September 5.

Front-month JKM rose to 11.345/MMBtu on Monday. It dropped to 11.330/MMBtu on Tuesday, and rose to 11.335/MMBtu on Wednesday.

State-run Japan Organization for Metals and Energy Security (Jogmec) said in a report earlier this week that JKM for last week “rose to mid-$11s/MMBtu on September 5 from low-$11s/MMBtu the previous weekend.”

“JKM rose to mid-$11s/MMBtu in the first half of the week due to uncertainty over possible sanctions referred from supplies from Russia’s Arctic LNG 2, but then fell back to low-$11s/MMBtu as the market adopted a wait-and-see approach. In the latter half of the week, JKM rose again to mid-$11s/MMBtu as spot demand increased in Japan amid the ongoing heatwaves,” Jogmec said.