")

This story requires a subscription

This includes a single user license.

Norwegian shipping firm Flex owns 13 LNG carriers, and these vessels mostly work under fixed-term charters.

The company’s vessel Flex Artemis is working on a variable hire charter, while Flex Constellation will be available for charter from the end of the first quarter of next year, as the current charterer decided not to exercise its one-year extension option.

Speaking on the company’s third-quarter earnings call on Tuesday, Kalleklev said, “we saw rates at around $85,000 in the middle of August, which is historically a good rate, but then the market fell off a cliff starting in September.”

“And we are now in a market which is pretty poor if you are looking at the spot market, but longer term, as evidenced also by the new contracts we are announcing, the market for longer-term demand is still very healthy,” he said.

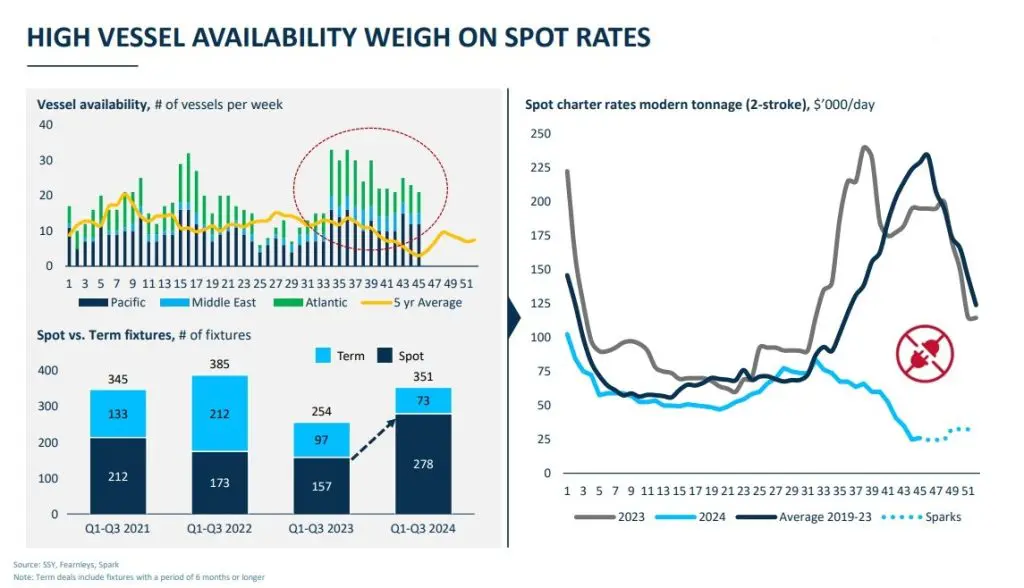

High number of LNG carriers

Kalleklev noted, “rates are softening, and they are down to very low levels, levels we have never really seen in the fourth quarter before.”

“And why is that? It’s really about the number of ships for delivery,” he said.

“And we see this in the upper left hand side with this red dotted bubble, where we see the number of ships available. So typically when you come to August, September, the market gets tighter,” he said.

“You might have floating storage if gas prices are in contango, meaning that they are higher later in the year than spot, which can typically drive up to 30, 40 ships in floating storage,” Kalleklev said.

“This year we have high gas prices, but they are not in contango. So it means you are disincentivized to do floating of the cargoes. So number of available ships have been building up, also with the scheduled deliveries of ships,” he said.

Kalleklev said this means that the market is “amply” supplied with LNG ships.

Rates around $25,000 for modern tonnage.

“Rather than picking up in September, (rates) have been going down right now at around $25,000 for modern tonnage. This means high fuel tonnage is at $10,000 and all the steamships are basically being priced out of the market,” Kalleklev said.

“With ample liquidity in the spot market in terms of number of ships, it’s not surprising also to see the charters leaning back, fixing ships on spot basis rather than term, with the numbers of spot voyages this year compared to the previous year, picking up a lot from 157 fixtures from Q1 to Q3 last year to 278 this year,” he said.

“So at least the spot market is liquid, but rates are poor, and we expect the market to stay poor for the remainder of the year,” he said.

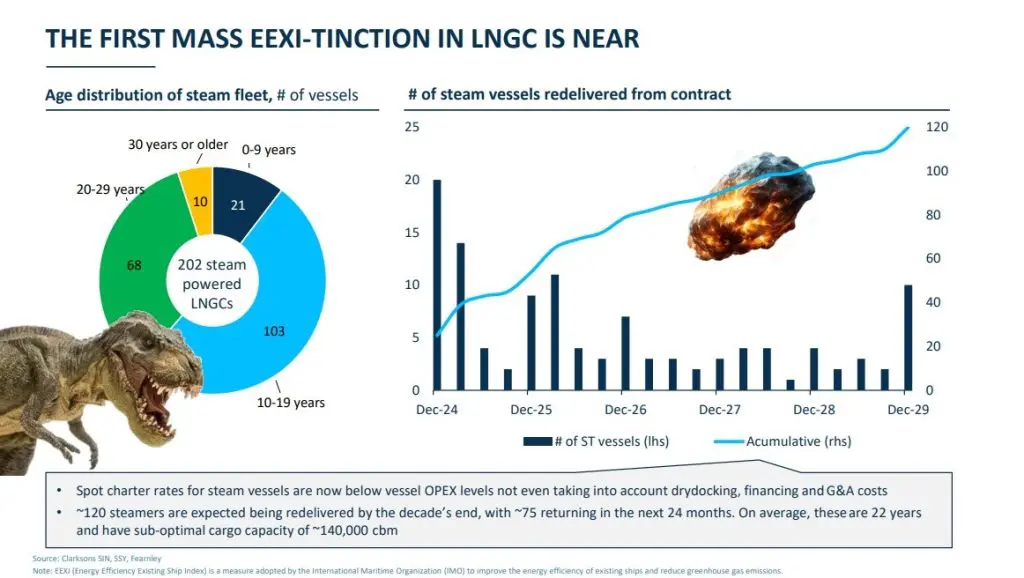

Steamships

He said this will have “some implications” for the steamships.

“We have said this in the past, that there’s been a huge technology change in terms of the ships. We started off this industry with steamships. Most people understand that steam power is not really efficient,” he said.

However, “we still have a lot of steamships in the market. In total, the fleet is around 200 ships,” he said.

“So we’ve put the different ships here in the pie chart with the dinosaur,” he said.

“There actually are 21 quite modern steamships. These are a bit more modern steam in terms of efficiency, but they are all having the disadvantage of having a very inefficient propulsion system,” he said.

“Why are they still in the market? Because a lot of these steamships were fixed on 20, 25-year charters, and they are rolling off these charters in the coming years, with about 75 of these ships being returned from long-term charters in the next 24 months,” he said.

“And we put up all the numbers of ships with redelivery dates there — in the chart, with the big asteroid hitting them,” he said.

“Mass EEXI-tinction”

“What we expect will happen here is a mass EEXI-tinction. So EEXI means Energy Efficiency for Existing Ships Index, which is part of the IMO rules to reduce greenhouse gas emissions for the shipping sector,” he said.

Kalleklev said these ships are now “technically and commercially obsolete, and we do think scrapping activity will take up, and which we do think will rebalance the market in 2027.”

He said that historically, there has been very limited scrapping demand.

“But as mentioned with all these steamships coming off charters, in this kind of market balance we assume 53 of the 75 ships to be removed from the market,” he said.

“This could be more if the market stays soft. It’s very expensive to take a steamship through a 25-year special survey,” he said.

“But in general, we see that the market is balancing out 27, 28, depending a bit on scrapping and depending a bit on these new export projects when they are coming to the market, whether there will be any delays and such,” he said.

Around 300 LNG carriers scheduled for delivery

He also touched upon the LNG carrier order book, saying there are “around 300 ships for delivery.”

“What we see is that there is a very limited number of uncommitted ships. Most of the ships at these prices are built towards a long-term contract,” he said.

“So of the 300 ships for the delivery, it’s only about 20 ships which are open. And as you see, when we’re getting to 2028 onwards, there’s really no speculative ordering because these prices are discouraging such contracting,” he said.

Kalleklev said that a lot of these ships are for Qatar.

QatarEnergy is currently working on the giant North Field LNG expansion program. This includes the North Field South and North Field West projects.

Together, these will raise Qatar’s LNG production capacity from the current 77 mtpa to 142 mtpa in 2030.

In February, QatarEnergy also announced the North Field West project which will add 16 mtpa of LNG to the expansion.

“So these are really ships for their new volumes and also for replacing some of the older steamships they have in their fleets,” he said.

“We also have a lot of non-Qatar vessels. These are related mostly to fleet renewal of the same ships as mentioned, but also for the new export projects coming out of US and other countries,” he said.