This story requires a subscription

This includes a single user license.

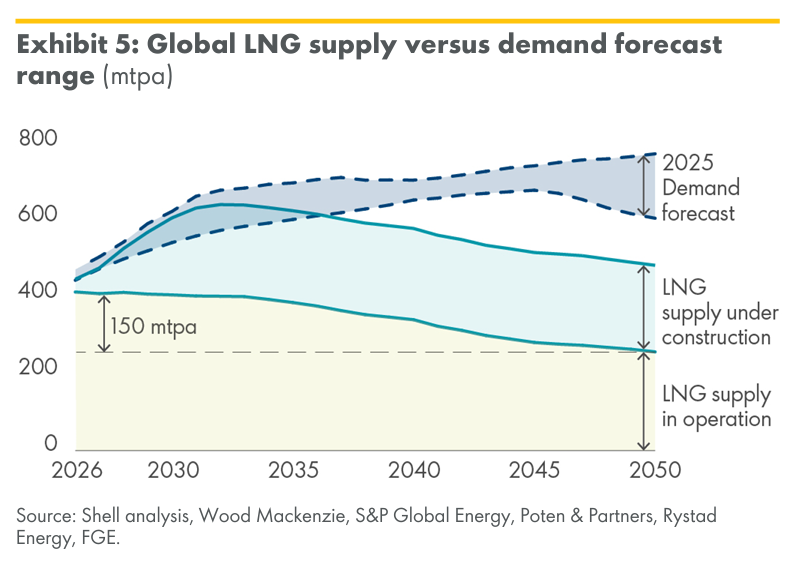

UK-based LNG giant Shell extended the forecast range to 2050 in its new report, named LNG portfolio strategic spotlight.

According to the company, global demand for LNG is expected to increase from 422 mtpa in 2025 to between 650 mtpa and 710 mtpa by 2040, or by around 54-68 percent.

In its 2025 LNG Outlook, Shell expected LNG demand to reach 630-718 million tonnes a year by 2040, a higher forecast than in the year before.

Shell said in the new report it expects that “much of the growth in LNG demand will take place in developing markets, particularly in Asia, where the use of natural gas is playing a critical role in lowering emissions.”

“In 2024, non-OECD Asian countries accounted for around 41 percent of global LNG imports, up from 26 percent in 2015. This increase happened even as Europe imported significantly more LNG to replace Russian pipeline gas starting in 2022,” Shell said.

Over the last decade, LNG imports into non-OECD countries grew at an annualised rate of close to 9 percent, while imports into OECD countries increased by less than 4 percent per year on average.

By 2050, forecasts indicate that almost 75 percent of LNG demand will come from non-OECD markets and the international maritime sector, Shell said.

Near-term LNG outlook

Shell noted that the LNG industry is in the early stages of a new investment supercycle.

A wave of new projects in the USA and Qatar’s North Field expansion are scheduled to add significant volumes from 2026 onwards.

As a result, the industry consensus is that the global LNG market will expand by almost 40 percent by 2030, from 422 mtpa in 2025, Shell said.

Shell said this expansion of the LNG market is expected to lead to a period of oversupply, with weaker prices.

However, the extent of a potential supply overhang is challenging to predict because of uncertainty around the timing of supply development, as individual projects regularly face delays because of supply chain and labour issues, it said.

These include projects sponsored by international and national oil companies.

Further uncertainty comes from geopolitics, the demand-side response, the performance of the gas fields feeding the LNG plants, the development of supporting infrastructure, supplier

strategies, new sectors and markets for LNG, and government policies and regulations, Shell said.

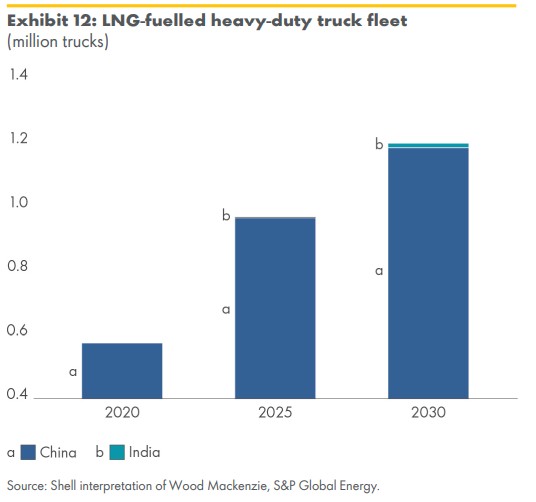

Almost 1 million LNG-powered vehicles in China

Shell noted that LNG is helping to decarbonise shipping by replacing oil and helping the sector to meet increasingly strict environmental regulations.

With more than 850 LNG-fuelled vessels already in operation, the global fleet could nearly double over the next five years, assuming current orderbook deliveries proceed as planned, Shell said.

The industry is also making progress in addressing methane emissions from engines.

More than 90 percent of LNG ships on order have less than 0.8 percent methane slip emissions, which refers to the release of unburned methane from engines that use LNG as a fuel, Shell said.

On the road, the use of LNG has “significantly” reduced transport emissions in China, where more than 20 percent of new heavy-duty trucks are fuelled by LNG today, according to Shell.

Shell said the total fleet of LNG-fueled vehicles is now almost 1 million vehicles in China, nearly 70 percent more compared with 2020.

The use of LNG-fuelled vehicles in India is just beginning, but could follow a similar trajectory to China of rapid adoption if supported by government policy, Shell noted.