This story requires a subscription

This includes a single user license.

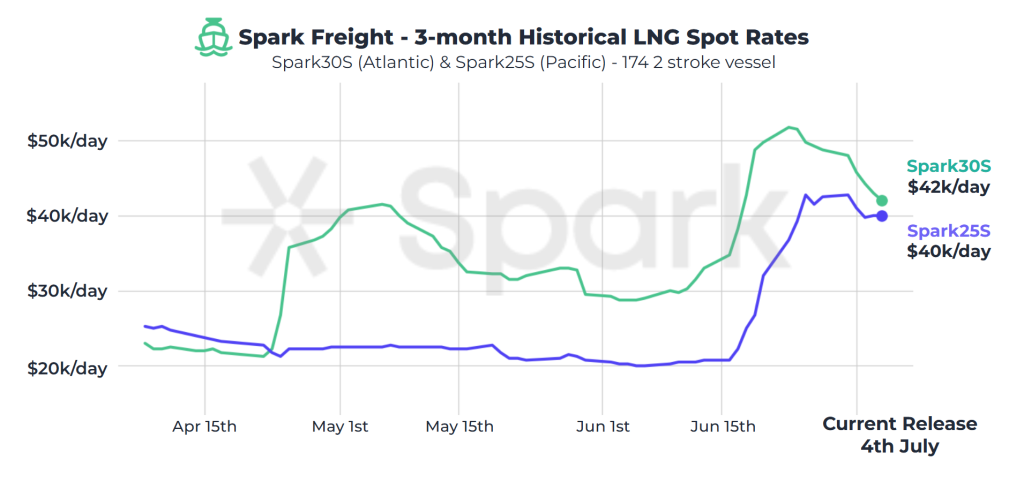

“Spark30S (Atlantic) freight rates fell sharply this week, dropping by $6,750 to $42,000 per day this week and the largest week-on-week decline since January,” Spark’s data lead Qasim Afghan told LNG Prime on Friday.

Similarly, Spark25S (Pacific) rates decreased by $2,500 to $40,000 per day, he said.

European prices down

In Europe, the SparkNWE DES LNG dropped compared to last week.

“The SparkNWE DES LNG front month price for August is assessed at $11.175/MMBtu,” Afghan said.

He said the basis to the TTF widened for the first time in nine weeks, assessed at $0.405/MMBtu, but still indicating reduced demand for LNG delivery slots in NW-Europe.

“The US front-month arb to NE-Asia (via the Cape of Good Hope) continues to marginally point to Europe, pricing in at -$0.109/MMBtu. The US front-month arb to NE-Asia via Panama continues to point to Asia for a fifth week running, assessed at $0.125/MMBtu,” Afghan said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU continued to rise and were 59.44 percent full on July 2.

Gas storages were 57.15 percent full on June 25, and 77.91 percent full on July 2, 2024.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in August 2025 settled at $13.160/MMBtu on Thursday.

Last week, JKM for August settled at 13.195/MMBtu on Friday, June 27.

Front-month JKM dropped to 13.125/MMBtu on Monday and to 13.105/MMBtu on Tuesday. It rose to 13.165/MMBtu on Wednesday.

State-run Japan Organization for Metals and Energy Security (Jogmec) said in a report earlier this week that JKM for last week “fell to mid-$12s/MMBtu on June 27 from high-$14s/MMBtu the previous weekend.”

“JKM rose to high-$14s/MMBtu on June 23 due to tensions in the Middle East, but subsequently continued to fall to mid-$12s/MMBtu as geopolitical tensions subsided with the announcement of an Israeli-Iranian ceasefire, and demand in Asia remained sluggish,” Jogmec said.