This story requires a subscription

This includes a single user license.

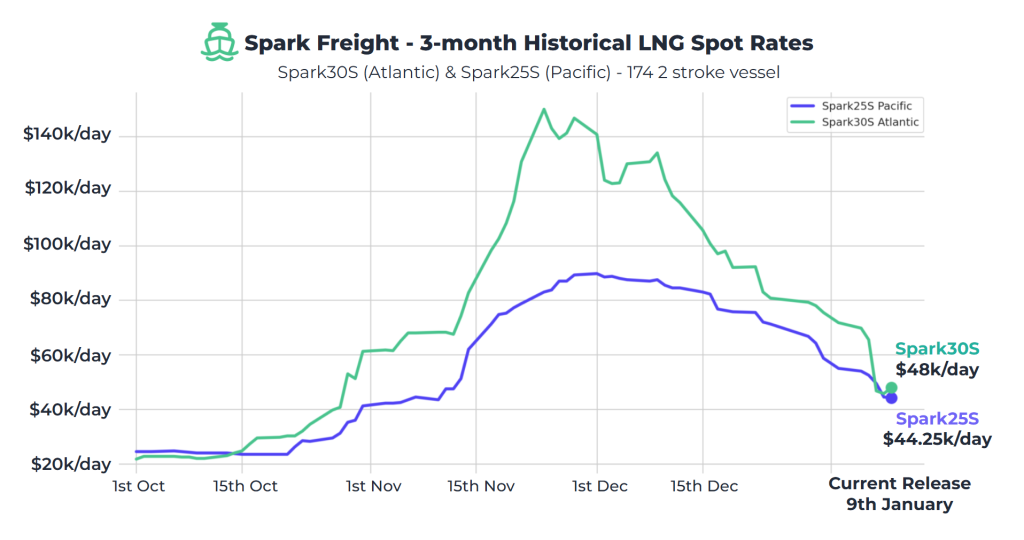

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) LNG freight rates decreased by $23,750 to $48,000 per day, the largest week-on-week decline since January 2024.

“Similarly, Spark25S (Pacific) rates decreased $10,750 to $44,250 per day,” he said.

“Barely a week into 2026, the LNG shipping market has already delivered some notable shifts. While geopolitical uncertainty continues to cloud the broader outlook, even a narrow focus on LNG freight offers plenty to unpack,” Fearnley LNG said in its weekly LNG report.

The Oslo-based advisory and brokering firm said that “sentiment has softened as several vessels have come open against a limited flow of fresh requirements.”

“Charterers have generally been comfortable holding back and, in some cases, have been rewarded with materially softer fixing levels. That said, the momentum may already be turning again, with a renewed wave of enquiries emerging and the market appearing more balanced on paper,” it said.

Fearnley LNG noted that the Pacific basin has followed a “more predictable path, with downward pressure translating into a steady easing in fixing levels, albeit from a lower base than the Atlantic.”

“Meanwhile, the Middle East remains more active than has traditionally been the case, although the build-up of tonnage is starting to weigh on ballast premiums,” it said.

“As attention turns to how the market absorbs a weaker environment into Q1, conditions are clearly cooling, but there is still some fight left in the market,” Fearnley LNG said.

European prices down

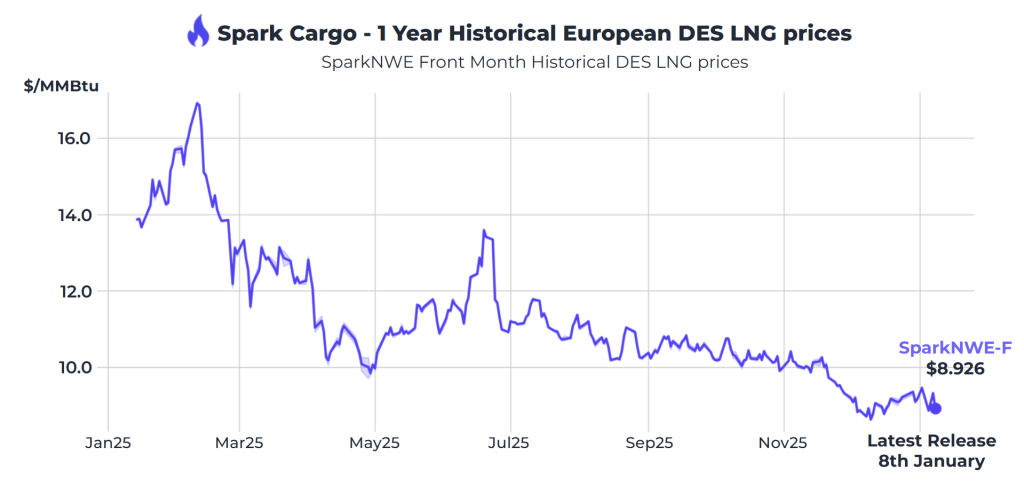

In Europe, the SparkNWE DES LNG decreased compared to last week.

“The SparkNWE DES LNG front-month price for February decreased $0.247 to $8.926/MMBtu, whilst the basis to the TTF is assessed at -$0.545/MMBtu,” Afghan said.

“The US front-month arb (via COGH) closed out further this week, currently assessed at -$0.349/MMBtu and more strongly pointing to Europe, driven by a recent fall in the JKM-TTF spread,” Afghan said.

“Similarly, the Nigerian front-month arb (via COGH) has closed out once again and is also pointing to Europe, assessed at -$0.005/MMBtu,” he said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU dipped from last week and were 57.18 percent full on January 7, 2026.

Gas storages were 62.67 percent full on December 30, 2025, and 68.84 percent full on January 7, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in February 2025 settled at $9.555/MMBtu on Thursday.

Last week, JKM for February settled at 9.700/MMBtu on Friday, January 2.

Front-month JKM dropped to 9.540/MMBtu on Monday. It rose to 9.575/MMBtu on Tuesday and 9.605/MMBtu on Wednesday.

State-run Japan Organization for Metals and Energy Security (Jogmec) said in a report earlier this week that JKM for the “last two weeks (December 22 – January 2, February delivery) rose to high-$9s/MMBtu on January 2 from mid-$9s/MMBtu the previous weekend (December 19).”

“During this period, JKM moved within a narrow mid-to-high-$9s/MMBtu range, weighed by thin liquidity and subdued demand amid the year-end and New Year holidays. While it saw temporary support from heightened geopolitical risks and the coldest weather of the winter in South Korea, spot demand, especially from China, remained weak, limiting the upside,” Jogmec said.