This story requires a subscription

This includes a single user license.

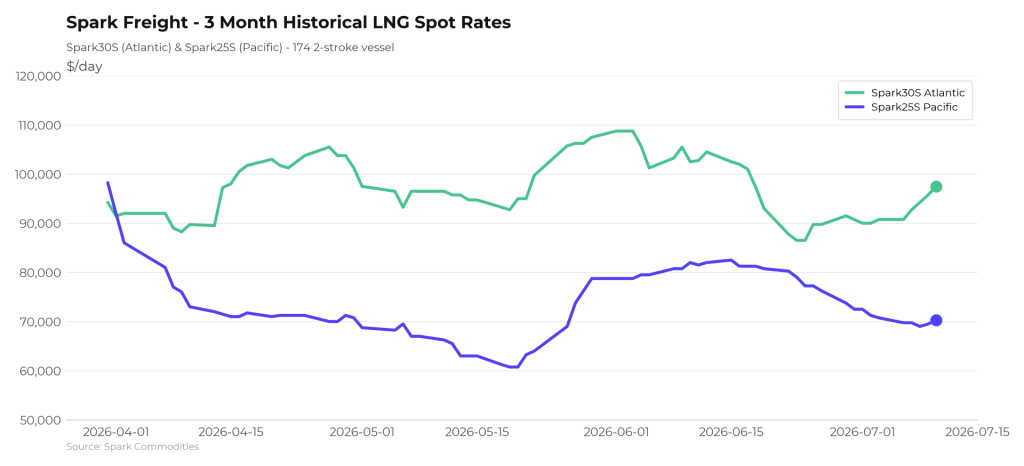

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) rates rose $6,750 week-on-week to $97,500 per day.

Afghan said that Spark25S (Pacific) rates have dropped a further $500 to $70,250 per day.

Middle East

“Renewed hostilities in the Middle East have put LNG directly in the firing line, but the freight market has held its nerve and spot rates remain broadly stable for now,” Fearnley LNG said in its weekly LNG report on Thursday.

“Steady fixing since the start of the month has eroded the long availability lists of recent weeks, and longer voyages driven by the open arbitrage have created some tightness in the early August window in the Atlantic,” the Oslo-based advisory and brokering firm said.

“Rates in the West are therefore increasing, albeit at a modest pace and still within the bounds we have seen in recent months. TFDEs in the East have seen some downward pressure, but levels for modern tonnage remain resilient, supported by firming DES prices and thinning availability,” Fearnley LNG noted.

According to Fearnley LNG, current availability is “concentrated on the prompt to mid-July, while demand on both sides of Suez sits early August onwards, leaving owners to absorb idle time to bridge the gap into their next employment.”

“In contrast to recent weeks, a broad spread of firm requirements is being worked, keeping all participants busy. Charterers continue to pay up for worldwide redelivery flexibility, with the economics of sending Atlantic cargoes East still justifying the premium,” Fearnley LNG added.

European demand

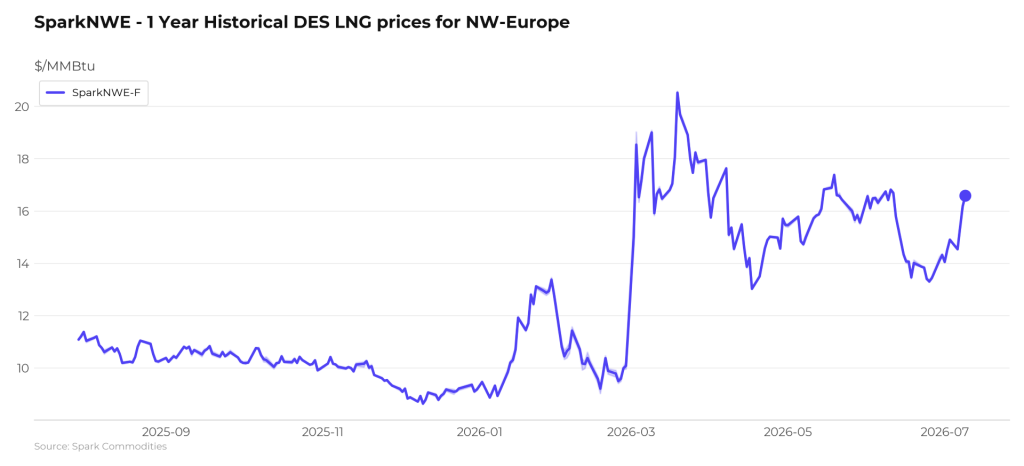

In Europe, the SparkNWE DES LNG rose compared to last week.

“The SparkNWE front month DES LNG price for August delivery is currently assessed at TTF-$0.200, narrowing 4.5c since last week. The outright NWE DES LNG price is now at $16.587/MMBtu, rallying $2.071 week-on-week and marking the largest week-on-week increase since mid-March,” Afghan said.

“Spark’s US Gulf Coast prompt LNG cargo valuation is priced at $15.225/MMBtu as of yesterday’s close, increasing $1.947 (+14.6 percent) week-on-week,” he said.

Moreover, Afghan said that “the US prompt (M+1) arb via COGH has widened $0.114 in favor of Europe, currently priced at -$0.478/MMBtu – the strongest signal to Europe since mid-March.”

“The US M+1 arb via Panama remains open and firmly pointing to Asia, now priced at +$0.505/MMBtu,” Afghan said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU rose from the previous week.

Gas storages were 51.10 percent full on July 9, 2026. The storages were 49.22 percent full on July 2, 2026, while the storages were 61.59 percent full on July 9, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in August 2026 settled at $16.575/MMBtu on Thursday.

Last week, JKM for August settled at 16.080/MMBtu on Thursday, July 2.

Front-month JKM dropped to 16.065/MMBtu on Monday. It rose to 16.175/MMBtu on Tuesday and dropped to 16.510/MMBtu on Wednesday.