This story requires a subscription

This includes a single user license.

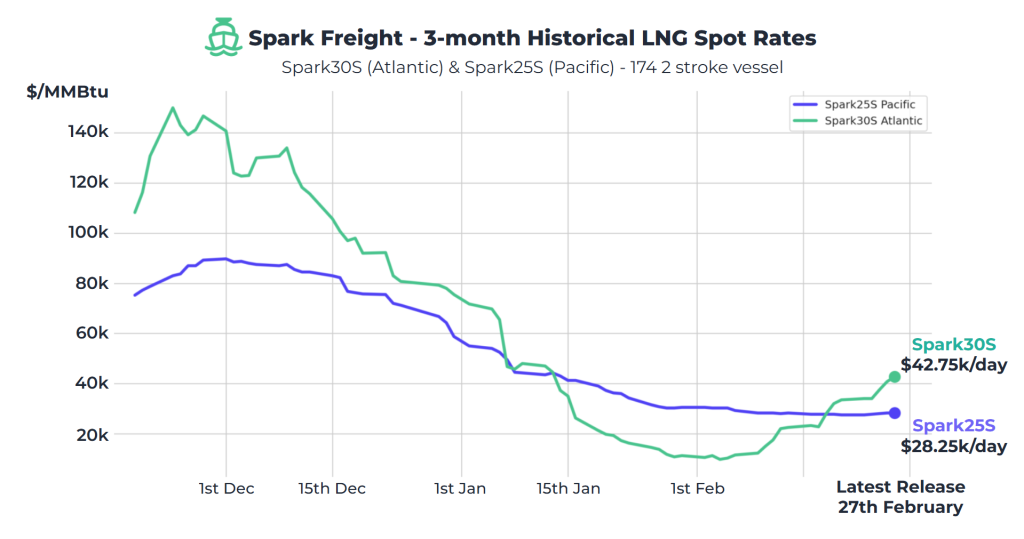

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) rose $9,250 to $42,750 per day this week.

He said Atlantic rates are up $32,250 since the beginning of February, and are $29,000 higher than rates seen this time last year.

“In contrast, Spark25S (Pacific) rates stayed relatively steady this week, assessed at $28,250 per day and continuing to remain tightly range-bound within a $3,000 range since the end of January,” Afghan said.

“The tale of two basins continues this week, as the delta between markets East and West of Suez widens,” Fearnley LNG said in its weekly LNG report.

The Oslo-based advisory and brokering firm said that in the Atlantic, “with off-takers working hard to mitigate recent weather-related disruptions, the market continues its climb through the $30k’s.”

“Consequently, as portfolios hold onto tonnage, there are some upcoming windows inthe West showing no availability at all,” it said.

“In the East, competition between owners and subletters for limited cargoes is giving charterers the edge in negotiating price. 2-stroke availability remains thin, but ample availability of TFDE’s and a relative lack of firm requirements sees levels struggling to keep up with the Atlantic,” Fearnley LNG said.

“While there is speculation over whether the spot market will correct as these disruptions unwind, the multimonth market for periods through summer suggests a higher floor than we saw in January,” Fearnley LNG said.

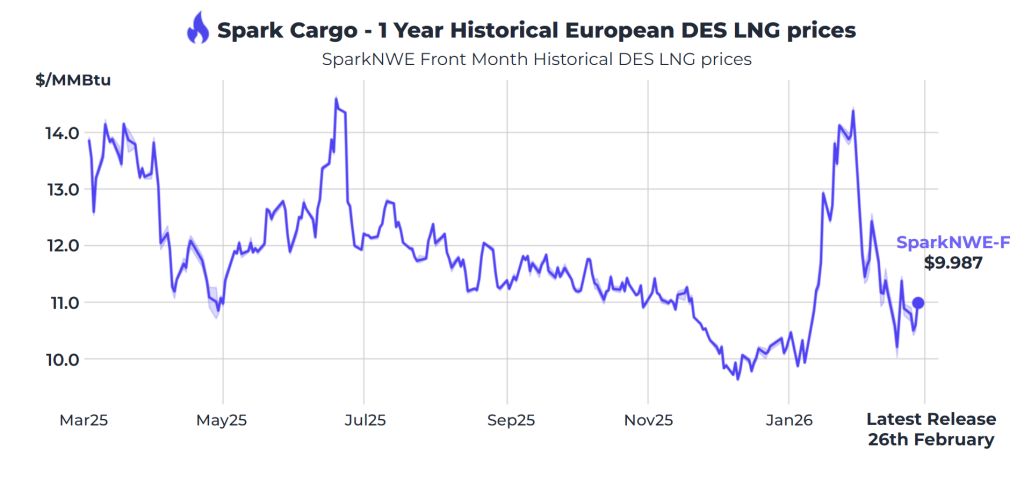

European prices down

In Europe, the SparkNWE DES LNG dropped compared to last week.

“The SparkNWE DES LNG front-month price for March dropped $0.384 this week to $9.987/MMBtu,” Afghan said.

He said that the basis to the TTF “is assessed at -$1.155/MMBtu, continuing to indicate significantly increased demand for delivery slots into NW-Europe.”

“The US front-month arb (via COGH) for March loading has narrowed further to -$0.194/MMBtu, but still continuing to point US prompt cargoes to Europe,” he said.

“Similarly, the Nigerian front-month arb (via COGH) has increased to $0.243/MMBtu and continues to point to Asia,” Afghan said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU dropped from last week and were 30.19 percent full on February 25, 2026.

Gas storages were 31.97 percent full on February 18, 2026, and 39.85 percent full on February 25, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in March 2026 settled at $10.605/MMBtu on Thursday.

Last week, JKM for March settled at 10.660/MMBtu on Friday, February 20.

Front-month JKM rose to 10.725/MMBtu on Monday. It dropped to 10.5200/MMBtu on Tuesday, and rose to 10.595/MMBtu on Wednesday.

Japan’s JOGMEC said in a report earlier this week that the Northeast Asian assessed spot LNG price JKM for last week “rose to low-$11s/MMBtu on February 20 from high-$10s/MMBtu the previous weekend.”

“JKM fell to mid-USD 10s/MMBtu at the beginning of the week due to weaker demand in the Asian market during the Lunar New Year holidays. In the latter half of the week, it rose because of increased purchases of spot cargoes in Northeast Asia and Southeast Asia. In Japan, demand increased due to unplanned outages at coal-fired power plants, while South Korea, Taiwan, and Thailand also actively procured spot cargoes. Meanwhile, some cargoes from West Africa and Australia were diverted to Europe, leading to a tightening supply-demand balance,” JOGMEC said.