This story requires a subscription

This includes a single user license.

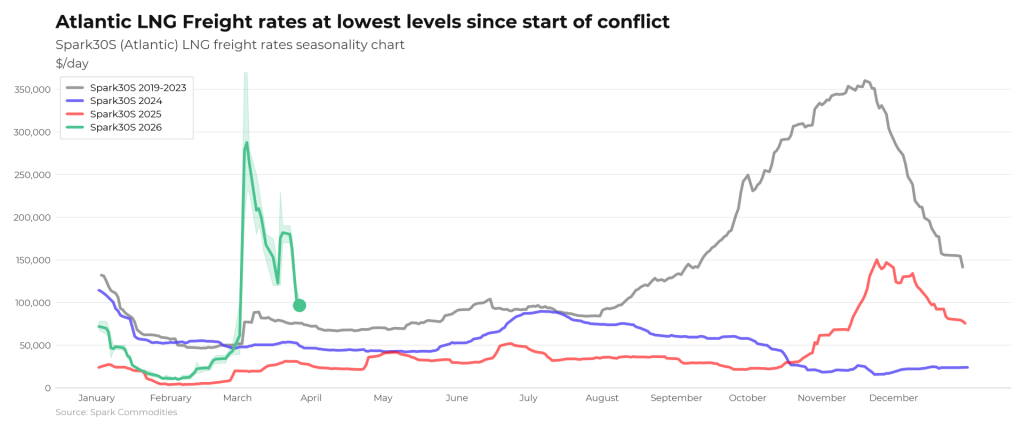

“Spark30S (Atlantic) rates have dropped $85,250 week-on-week, now at $96,500 per day – the lowest rates since the outbreak of the conflict (2nd March) and largely driven by the US front-month arb to Asia being firmly closed and pointing to Europe for the past week, incentivising US cargos to remain within the Atlantic basin and thus increasing vessel availability,” Spark’s data lead, Qasim Afghan, told LNG Prime on Friday.

He said Spark25S (Pacific) rates have dropped $33,750 to $108,000 per day.

“More stability”

“While conflict in the Middle East remains far from resolved, there is at least more stability in the prompt LNG commodity and freight markets this week,” Fearnley LNG said in its weekly LNG report on Thursday.

The Oslo-based advisory and brokering firm noted that shipping has “remained largely secondary to commodity price, and although swings in LNG DES levels have determined the direction of traffic to some extent, high freight rates have limited a full and sustained opening of the US-Asia arbitrage.”

“Despite fixing levels still being well above this year’s pre-conflict outlook, the apparent easing of the initial shock has given rise to a softening of sentiment across the board. Prompt vessels are competing more aggressively for employment, giving charterers more leverage in negotiations,” Fearnley LNG said.

Fearnley LNG said it remains to be seen whether the market is resilient enough to maintain levels above long-term breakeven; however, in the short term, it does appear that elevated cargo prices are supporting healthier freight levels.

“Looking beyond, the uncertainty in when or how the conflict will end, how production will be affected in the Middle East, and the future direction of trade flows are causing headaches in pricing longer-term charters. Although owners are there to lock in longer periods, the lack of clarity is impeding activity in the multimonth space,” it said.

“Forward availabilities provide even larger and perhaps sharper headaches for charterers, who wrestle with the risk of remaining short versus locking in flexibility at a premium to their now-outdated forecasts,” Fearnley LNG said.

Increased demand for delivery slots into NW-Europe

In Europe, the SparkNWE DES LNG dropped compared to last week.

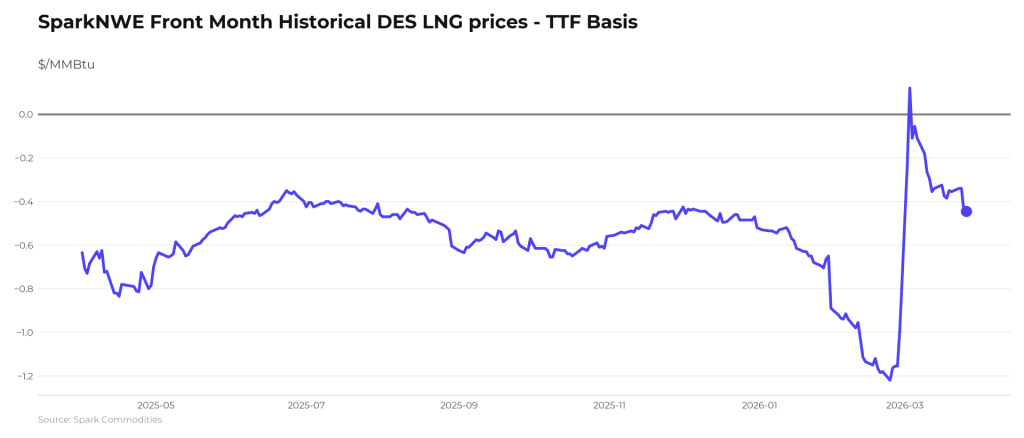

“The SparkNWE front-month DES LNG price for April delivery, assessed as a basis to the TTF, has widened 9.5c to TTF – $0.445 for NW-Europe front month delivery, indicating increased demand for delivery slots into NW-Europe,” Afghan said.

“The outright NWE DES LNG price is down $2.289 to $18.232/MMBtu, largely driven by a drop in TTF prices this week. This has been reflected across the forward curve as well, with May 2026 (M+2) to March 2027 (M+11) prices down approx. $1-$2, albeit still valued higher than levels seen before the strike on the Ras Laffan terminal last Thursday,” he said.

Afghan said that the JKM-TTF June 2026 spread is down 0.450 to $1.225/MMBtu.

TTF May 2026 prices are “down -$1.259 week-on-week, currently at $18.763/MMBtu.”

“The prompt (M+1) arb to Asia via COGH remained firmly closed this week, currently priced at -$0.373/MMBtu and pointing to Europe. The forward curve remains closed and pointing to Europe,” he said.

“The prompt (M+1) arb to Asia via COGH has seen strong volatility this week, opening and closing to Asia several times this week as JKM & TTF prices reacted to conflicting reports of progress in the Middle East. The prompt arb is currently open and pointing to Asia, priced at +$0.465/MMBtu,” Afghan said.

Gas storage

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU dropped from last week and were 28.44 percent full on March 26, 2026.

Gas storages were 28.66 percent full on March 19, 2026, and 33.65 percent full on March 26, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in May 2026 settled at $20.495/MMBtu on Thursday.

Last week, JKM for May settled at 21.705/MMBtu on Friday, March 20.

Front-month JKM dropped to 21/MMBtu on Monday, 20.525/MMBtu on Tuesday, and 19.990/MMBtu on Wednesday.

Australian LNG production

Several reports said on Friday that Chevron Australia was working to restore production at its Gorgon and Wheatstone LNG facilities in Western Australia following outages likely caused by Tropical Cyclone Narelle.

Woodside also reportedly said that production at its Karratha gas plant had been disrupted by the cyclone.