This story requires a subscription

This includes a single user license.

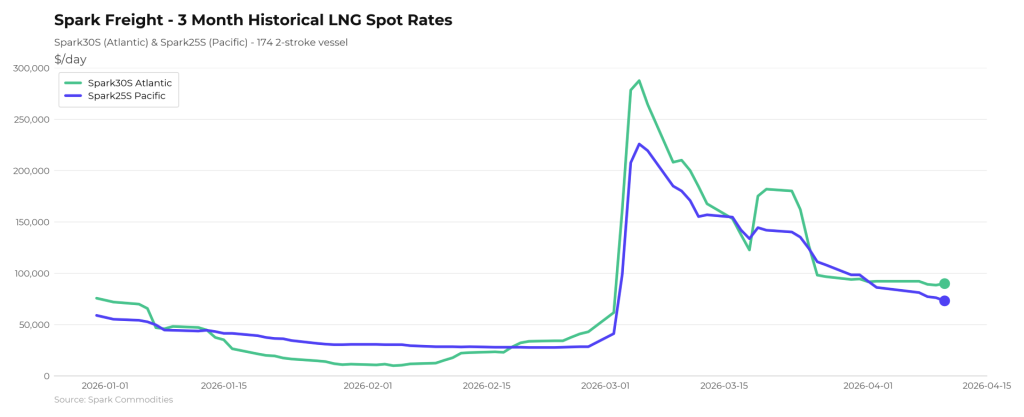

“Spark30S (Atlantic) rates have remained relatively steady this week, dropping $2,250 since last week and now at $89,750 per day,” Spark’s data lead, Qasim Afghan, told LNG Prime on Friday.

He said Spark25S (Pacific) rates have dropped $13,000 to $73,000 per day.

Slow process

UK-based Wood Mackenzie expects that if QatarEnergy began restarting its giant Ras Laffan LNG complex at the start of May, it would take until the end of August for the 12 trains to return to full service.

According to WoodMackenzie, a two-week ceasefire in the Middle East is bearish for global gas prices, but little has fundamentally changed with regards to LNG supply.

“If the present path of de-escalation is maintained, the energy and freight markets should return to normality, but it will be a slow process and the impact and outcome on LNG shipping dynamics remains uncertain,” Fearnley LNG said in its weekly LNG report on Thursday.

The Oslo-based advisory and brokering firm noted that in the coming weeks, “much will depend on the demand profiles across different regions, and whether Middle East facilities are able to commence what will be a slow and complex return to production.”

“In the Atlantic basin, a lack of prompt firm requirements is contributing to a softer rate sentiment, particularly as vessel availability builds through April and into 1H May. With limited liquidity, the market remains reactive, with participants trying to capture arbitrage opportunities or awaiting the next batch of cargoes,” Fearnley LNG said.

“Although there have been few opportunities, the East of Suez has seen comparatively stronger fixture activity over the holiday period. This has created a competitive environment, particularly for owners of TFDE tonnage. Combined with a growing list of open vessels, sentiment has softened, and players will be tracking markets carefully for clues as to how the market will develop as the ceasefire ensues,” it said.

Continued demand for delivery slots into NW-Europe

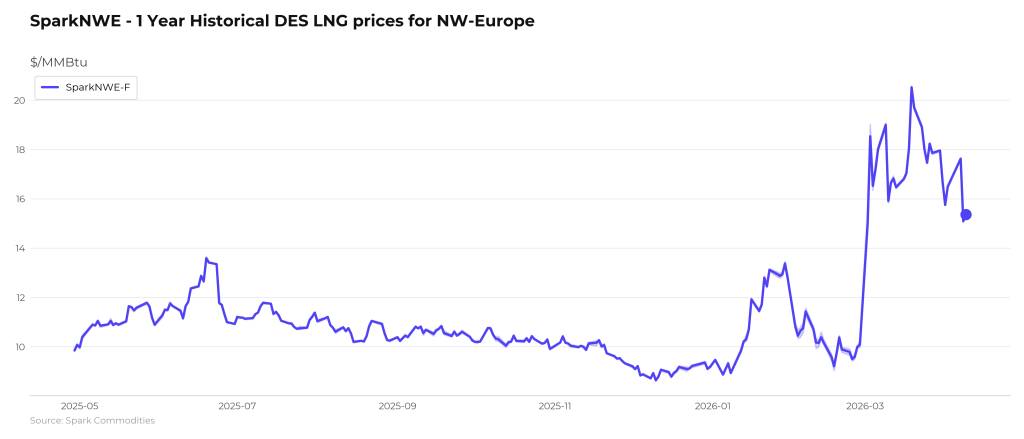

In Europe, the SparkNWE DES LNG dropped compared to last week.

“The SparkNWE front-month DES LNG price for May delivery is assessed at TTF-$0.450, indicating continued demand for delivery slots into NW-Europe,” Afghan said.

“The outright NWE DES LNG price is now at $15.362/MMBtu, the lowest front-month DES LNG price since the beginning of the Iran conflict (2nd March),” he said.

Afghan said that “the US prompt (M+1) arb to Asia via COGH is now pointing to Asia at +$0.173/MMBtu, driven by a reduction in May 2026 freight rates and a rally in the JKM-TTF premium – this marks the strongest signal to Asia since the strikes on Ras Laffan.”

“The US arb via Panama remains open and firmly pointing to Asia at +$0.731/MMBtu,” he said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU rose from last week and were 29.92 percent full on April 9, 2026.

Gas storages were 27.92 percent full on April 2, 2026, and 34.29 percent full on April 9, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in May 2026 settled at $19.495/MMBtu on Thursday.

Last week, JKM for May settled at 19.965/MMBtu on Thursday, April 2.

JKM was not updated on April 3 and April 6 due to Easter holidays.

Front-month JKM dropped to 19.865/MMBtu on Tuesday and 19.490/MMBtu on Wednesday.