This story requires a subscription

This includes a single user license.

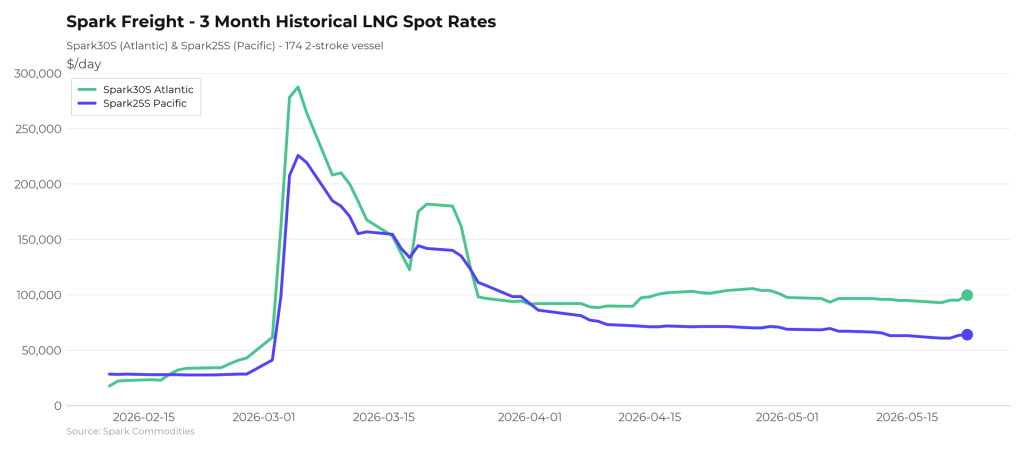

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) rates rose $5,000 to $99,750 per day this week, the first week-on-week increase in four weeks.

Afghan said Spark25S (Pacific) rates rose $1,000 to $64,000 per day, the first week-on-week increase in 10 weeks.

According to Afghan, Spark’s latest Atlantic FFA forward curve assessment shows a “largely flat structure for the rest of the year, with rates range-bound between $80,000-$95,000.”

“Fourth-quarter 2026 rates continue to rise and are at their highest levels yet, increasing $30,000 since the start of the war and now priced at $89,250,” he said.

New prompt requirements

“The Atlantic market showed early signs of a typical summer slowdown, partly due to a build-up of prompt tonnage after production issues at Freeport. That softer tone was short‑lived: new prompt requirements, including extra production from West and North Africa, tightened vessel availability at the front end,” Fearnley LNG said in its weekly LNG report on Thursday.

“Overall rates remain firm. A few fixtures were done at small discounts where availability was tighter, but these are exceptions. Charterers are often willing to pay a premium to secure operational flexibility, especially for multi‑voyage work or redelivery into Asia,” the Oslo-based advisory and brokering firm said.

Fearnley LNG said that “the prompt forward curve is supported, though visibility further out is limited.”

“There is clear interest in covering positions over the next two quarters, but the lack of significant 12‑month bids shows caution. This has produced a notable backwardation extending into 2027,” Fearnley LNG said.

“Beyond the near term, the outlook is highly uncertain. Geopolitical developments — notably ongoing disruptions around the Strait of Hormuz — could create further volatility. At the same time, the global gas supply balance is under close watch, as several typically quiet buying regions are expected to return ahead of peak demand in the second half of the year,” it said.

Continued reduced demand for delivery slots in Northwestern Europe

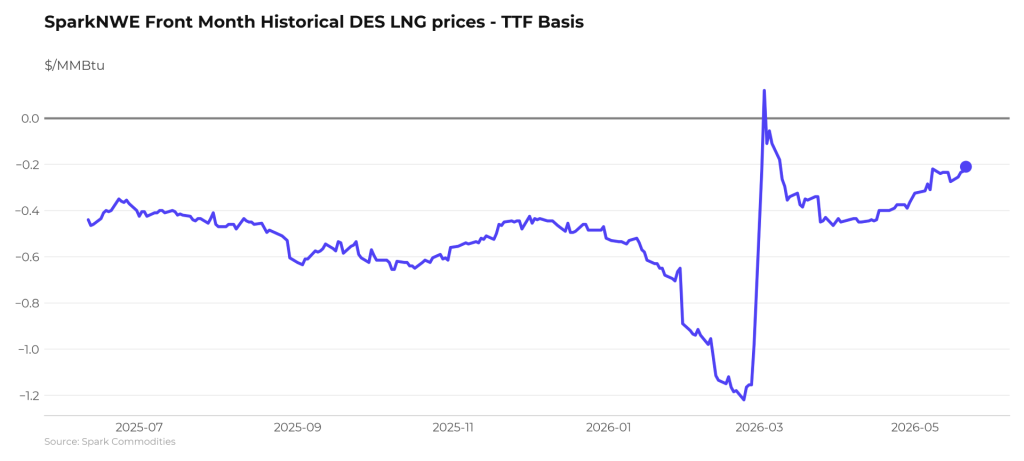

In Europe, the SparkNWE DES LNG rose compared to last week.

“The SparkNWE front-month DES LNG price for June delivery is assessed at TTF-$0.210, the narrowest discount in over two months and indicating further reduced demand for European delivery slots. The outright NWE DES LNG price is now at $16.577/MMBtu,” Afghan said.

“The US prompt (M+1) arb to Asia via COGH remains open and priced at +$0.161/MMBtu, marking a third consecutive week of pointing US prompt cargoes to Asia,” he said.

Afghan added that “the US M+1 arb via Panama remains open and firmly pointing to Asia for a twelfth week running, now priced at +$0.976/MMBtu.”

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU rose from last week and were 36.99 percent full on May 21, 2026.

Gas storages were 35.85 percent full on May 14, 2026, and 45.16 percent full on May 21, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in July 2026 settled at $18.920/MMBtu on Thursday.

Last week, JKM for June settled at 17.105/MMBtu on Friday, May 15.

Front-month JKM rose to 18.960/MMBtu on Monday, 19.615/MMBtu on Tuesday, and dropped to 18.905/MMBtu on Wednesday.