This story requires a subscription

This includes a single user license.

North America and the Middle East drove almost all of the supply growth thanks to the ramp-up of new liquefaction plants (North America) and better operations at legacy projects (Middle East), IEA said in tis latest quarterly gas market report.

On the import side, Europe took in more than the volume of incremental supply as Asian importers, led by China, significantly pared back their imports.

IEA said these trends are set to continue during the rest of 2025, with full-year LNG supply growth expected to reach 5.5 percent, or 30 bcm, as new projects continue to come online and ramp up production.

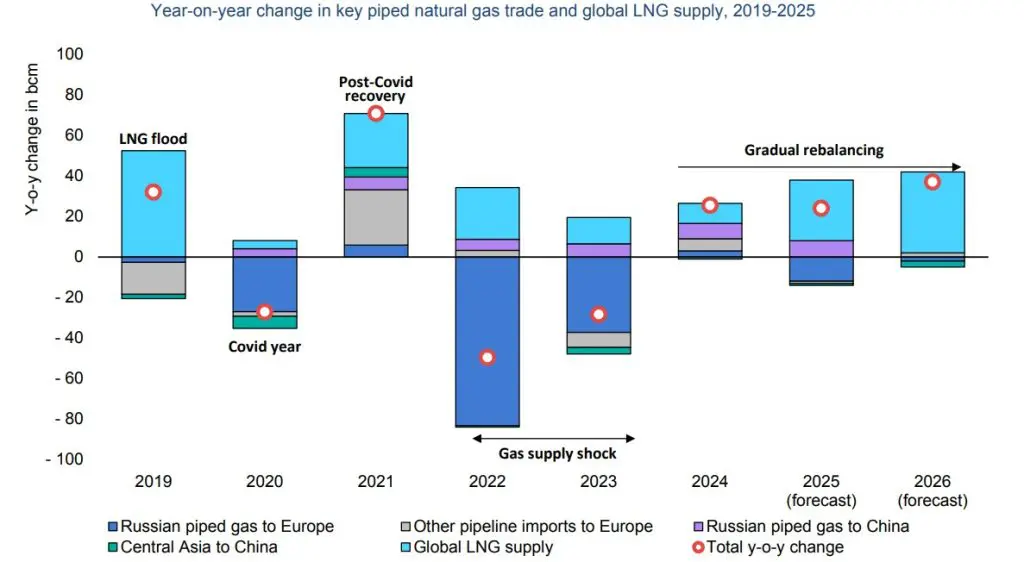

Europe’s increased call on the market is also set to continue as the continent balances lower Russian pipeline flows compared with 2024.

As a result, despite accelerated supply growth, interbasin competition for LNG volumes is expected to remain high, maintaining downward pressure on Asian LNG imports, the agency said.

North American exports to drive growth

The vast majority of incremental LNG supply in 2025 is set to come from North America, and the US in particular.

In the US, Venture Global Plaquemines LNG Phase 1 (18 bcm nameplate capacity) added nearly 8 bcm of LNG to the global balance in its first six months of operations, IEA said.

Coupled with improved operations at the existing Freeport LNG plant (which had suffered outages in the first half of 2024) and smaller incremental volumes from the Corpus Christi expansion, total US LNG supply growth reached over 12 bcm, or 21 percent, in the first half of 2025, IEA said.

Moreover, the agency said that NFE’s Fast LNG Altamira Train 1 in Mexico has already added much of its potential upside to the market in the first half of 2025 (having started exports in third-quarter 2024) and is expected to continue exporting steady volumes in the second half of 2025.

Canada’s eponymous liquefaction project, LNG Canada (19 bcm nameplate capacity), led by Shell, loaded its first cargo on June 30 and is set to add to supply growth in the second half of the year.

In total, combined LNG exports from Canada, Mexico, and the US are set to grow by an impressive 27 percent, or 32 bcm, in 2025, more than the continent’s incremental supply from the past three years combined, IEA said.

Qatar growth

Outside North America, Qatar is the only supply market to have shown notable growth in the first half of 2025, increasing its exports by about 5 bcm, or 9 percent, attributable to operational improvements and a likely delay in regular maintenance, IEA said.

Despite these bullish factors, a number of markets saw a decline in their exports over this period for a total setback of more than 8 bcm.

Most notably, Algerian LNG exports were down by 23 percent, or nearly 2 bcm, in the first half of 2025 as strong domestic demand compounded uncertain upstream dynamics.

Although exports showed a modest quarter-on-quarter recovery in Q2 2025, the underlying domestic market fundamentals at play are likely to maintain bearish pressure on exports in the second half of the year, according to the agency.

Russian supply declined by 7 percent, or 1.6 bcm, attributable mostly to sanctions halting exports at the country’s two small-scale plants (Portovaya LNG and Vysotsk LNG) from late February, IEA said.

Europe drives intensified competition for LNG volumes

The vast majority of LNG import growth in the first half of 2025 was concentrated in Europe, with Africa and the Middle East taking in smaller, yet relatively significant, incremental volumes, IEA said.

Combined, the increased call from these three regions was nearly double the volume of net incremental LNG supply over this period.

As a result, imports into Asia and Latin America contracted, marking a clear shift from the overarching trends of 2024.

European LNG imports grew by 25 percent (or almost 20 bcm) in the first half of the year, as the region sought to balance its supply mix following the expiry of the Ukrainian pipeline transit agreement for Russian gas (at the end of 2024) and lower pipeline flows from Norway.

IEA sid that Türkiye and the United Kingdom accounted for over one-quarter of this upside, concentrated mostly in the winter months, in line with both countries’ highly seasonal import patterns.

While EU imports were also up in the first quarter of 2025, this growth was most notable during March-June, driven by increased underground gas storage injection requirements to recover from below-average endof-winter levels.

In total, Europe is expected to import 26 percent (or 35 bcm) more LNG in the whole of 2025 as both demand and storage injections remain above 2024 levels and piped gas supplies ease.

This stands in stark contrast to the 18 percent (or 29 bcm) decrease in European LNG

imports in 2024, IEA said.

Short-term risks to the 2025 outlook

Despite accelerated LNG supply growth this year, strong crossbasin competition for cargoes means that the market remains vulnerable to unexpected shocks, IEA said.

The agency said that “military strikes in the Middle East led to Israel turning down its offshore gas production in June.”

“Although production has since resumed, any further outages in the Eastern Mediterranean would weigh on the region’s gas balance, driving increased LNG imports in markets such as Egypt,” it said.

Furthermore, close to 20 percent of global LNG supply transits through the Strait of Hormuz.

“No disruptions occurred at this key global energy transit point during the June Israel-Iran military conflict, but flare-ups in the region elevate the risk of potential disruption to global LNG flows,” IEA said.

Finally, while new liquefaction projects are set to bring further incremental volumes to market in the second half of the year, any unexpected hiccups in the start-up and ramp-up schedules of these plants would effectively tighten the global LNG balance, IEA said.

A widening liquefaction wave in 2026

While 2025 marks the start of the next wave of new liquefaction projects coming online in the second half of this decade, incremental capacity additions in 2026 are expected to be about

60 percent greater than in 2025, IEA said.

North America is set to account for the lion’s share of this incremental capacity, with Qatar also accounting for a significant share.

As a result of this new liquefaction capacity, global LNG supply is expected to grow by 7 percent, or about 40 bcm, in 2026, the largest annual upside – in both volumetric and percentage terms – since 2019, IEA said.

The US, Canada and Mexico together are expected to account for over 70 percent of total global incremental capacity in 2026.

US additions will be largely driven by the start of Golden Pass LNG, but a spillover effect from projects starting in 2025 and working toward full utilisation 2026 will also contribute to supply upside.

As such, Plaquemines LNG and Corpus Christi Stage 3 expansion are also set to contribute to incremental LNG exports in 2026, much like LNG Canada.

In Mexico, Sempra Infrastructure’s Energia Costa Azul LNG (about 4 bcm/yr nameplate capacity) is expected to come online in 2026, further boosting LNG supply from the Atlantic Basin.

Qatar’s North Field East project is set to start exports in 2026, although much of its expected upside will spill into 2027.

Asian LNG imports to grow

On the demand side, the wave of LNG supply is set to allow a return to more significant import growth across a number of countries that are expected to dial back their buying in 2025, IEA said.

Asian LNG imports are set to grow by about 10 percent in 2026.

China, the world’s largest LNG importer, is expected to act as the primary growth factor, swinging from an anticipated 11 percent LNG import contraction in 2025 to 25 percent (23 bcm) growth in 2026, IEA said.

Combined LNG import growth from smaller and emerging Asian markets, including India, is expected to reach about 19 percent (or 17 bcm).

Among the more mature Asian importers, Japan is set to decrease its take as nuclear start-ups reduce power sector gas burn, but Korea is likely to maintain relatively steady LNG imports, IEA said.

The agnecy said that Europe’s LNG imports are expected to marginally decline amid lower domestic demand and higher piped gas deliveries from Norway.

African imports are set to remain high as Egypt’s gas balance remains tight, and growing adoption of gas use in the Middle East continues to drive LNG import growth of about 15 percent in the region, IEA said