This story requires a subscription

This includes a single user license.

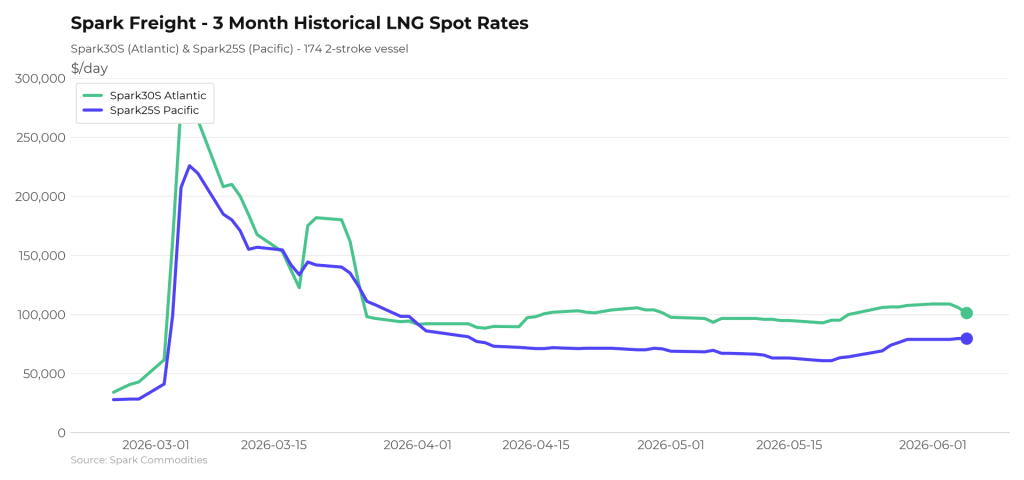

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) rates fell $6,250 to $101,250 per day.

Afghan said Spark25S (Pacific) rates remained relatively steady, rising $750 to $79,500 per day.

“Atlantic market looks increasingly tight for July”

“Rates continue to stay buoyant across the basins, as both Atlantic and Pacific markets enjoy increased liquidity over spot and term periods,” Fearnley LNG said in its weekly LNG report on Thursday.

“Several competing requirements in the East for 2H June have made availability among TFDEs appear tight for the first time in some weeks, which is reflected by gently increasing headline rates. The Atlantic market looks increasingly tight for July, driven mainly by sustained arbitrage pulling ships out of the intra-basin trade flows to which we have become accustomed,” the Oslo-based advisory and brokering firm said.

Furthermore, Fearnley LNG said that “the steady flow of multi-month fixtures continues for another week, as players remain eager to take on additional coverage and optimize fleets through Q3.”

“These patterns show little sign of slowing down, as both developing and firm requirements for 1H July have already hit the market. Layer on to the current market dynamics the continuing difficulties resolving the conflict in the Middle East, and the firmness we’re seeing today looks set to persist for the foreseeable future,” Fearnley LNG said.

Continued reduced demand for European delivery slots

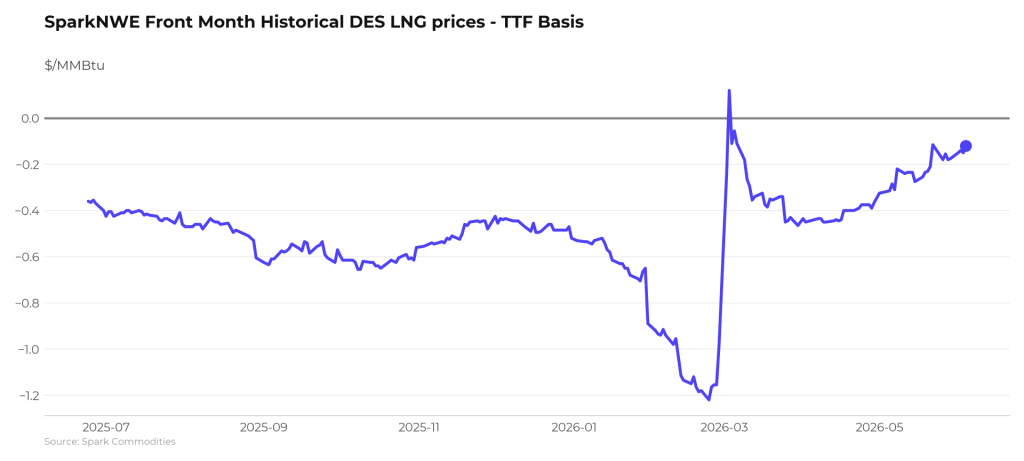

In Europe, the SparkNWE DES LNG rose compared to last week.

“The SparkNWE front-month DES LNG price for July delivery has narrowed to TTF-$0.120, indicating further reduced demand for European delivery slots. The outright NWE DES LNG price is now at $16.497/MMBtu, rising $0.660 week-on-week,” Afghan said.

Moreover, “on Monday, the US prompt (M+1) arb to Asia via COGH briefly closed out and was pointing to Europe for the first time in a month – the arb has since opened up to Asia again albeit marginally, now priced at $0.055/MMBtu,” he said.

Afghan added that “the US M+1 arb via Panama remains open and firmly pointing to Asia, now priced at +$0.973/MMBtu.”

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU rose from the previous week.

Gas storages were 41.25 percent full on June 4, 2026. The storages were 39.13 percent full on May 27, 2026, while the storages were 49.55 percent full on June 4, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in July 2026 settled at $18.765/MMBtu on Thursday.

Last week, JKM for July settled at 18.300/MMBtu on Friday, May 29.

Front-month JKM rose to 18.685/MMBtu on Monday. It dropped to 18.610/MMBtu on Tuesday and rose to 18.815/MMBtu on Wednesday.