This story requires a subscription

This includes a single user license.

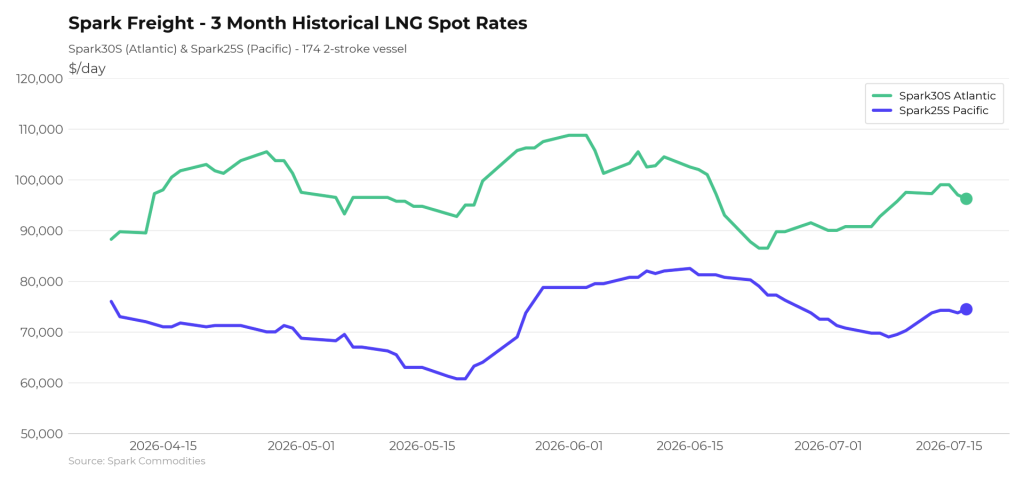

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) rates decreased $1,250 week-on-week to $96,250 per day.

Afghan said that Spark25S (Pacific) rates increased $4,250 to $74,500 per day.

Geopolitical uncertainty persisting

“The Atlantic market strengthened further during the week, with modern 2-stroke rates pushing towards the $100,000/day mark and TFDE tonnage from the East seen covering outstanding Atlantic requirements in the first half of August,” Fearnley LNG said in its weekly LNG report on Thursday.

“Availability appears healthy but is typically tighter once flexibility between basins is required. A growing theme is the disconnect between spot freight rates and cargo economics, with the same flexibility sought by FOB buyers also attracting a premium on the cargo side,” the Oslo-based advisory and brokering firm said.

“The Pacific has seen one of its busiest weeks in recent memory with fixtures East of Suez touching double digits, although rates have so far remained relatively contained,” Fearnley LNG noted.

According to Fearnley LNG, activity from West Africa has also “picked up noticeably.”

“While it is too early to determine whether this signals a repeat of the production growth that drove the market higher in Q4-25, it is a development worth monitoring,” Fearnley LNG said.

“Looking ahead, the balance of the year remains backwardated with multimonth interest increasingly price sensitive as availability builds and both owners and subletters seek coverage into 2027,” it said.

“For the traditionalists, the idea of Winter trading at a discount to Summer remains difficult to reconcile. With geopolitical uncertainty persisting, and in some regard increasing, there remains a credible case behind both sides of the bid-offer spread,” Fearnley LNG added.

TTF jumps

In Europe, the SparkNWE DES LNG jumped compared to last week.

“TTF prices have risen significantly over the last week, as the situation in the Middle East continues to escalate. TTF Sep26 contract has increased $2.696 (16.4 percent) to $19.088/MMBtu, the highest levels for that contract since March. The Oct26 JKM-TTF contract has increased +0.500 to $1.325 – the highest JKM premium to the TTF so far for the Oct26 contract, albeit still over 50c too narrow to flip the US prompt arb to signal to Asia instead of Europe for August loading cargoes,” Afghan said.

“The SparkNWE front month DES LNG price for August delivery is currently assessed at TTF-$0.155, narrowing another 4.5c since last week and indicating reduced demand for delivery slots in NW Europe. The outright NWE DES LNG price is now at $18.218/MMBtu, rallying $1.631 week-on-week and now at the highest levels since March,” he said.

Moreover, Afghan said that “Spark’s US Gulf Coast prompt LNG cargo valuation is priced at $16.794/MMBtu as of yesterday’s close, increasing $1.569 (+10.3 percent) week-on-week and now at the highest levels since mid-March.”

“The US prompt (M+1) arb via COGH narrowed by $0.201, currently priced at -$0.277/MMBtu and still pointing to Europe, albeit the weakest signal to Europe since July 1. The US M+1 arb via Panama remains open and firmly pointing to Asia, now priced at +$0.731/MMBtu,” Afghan said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU continued to rise.

Gas storages were 53 percent full on July 16, 2026. The storages were 51.10 percent full on July 9, 2026, while the storages were 63.61 percent full on July 16, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in September 2026 settled at $19.925/MMBtu on Thursday.

Last week, JKM for August settled at 16.520/MMBtu on Thursday, July 10.

Front-month JKM rose to 16.530/MMBtu on Monday, 16.530/MMBtu on Tuesday, and 16.808/MMBtu on Wednesday.