This story requires a subscription

This includes a single user license.

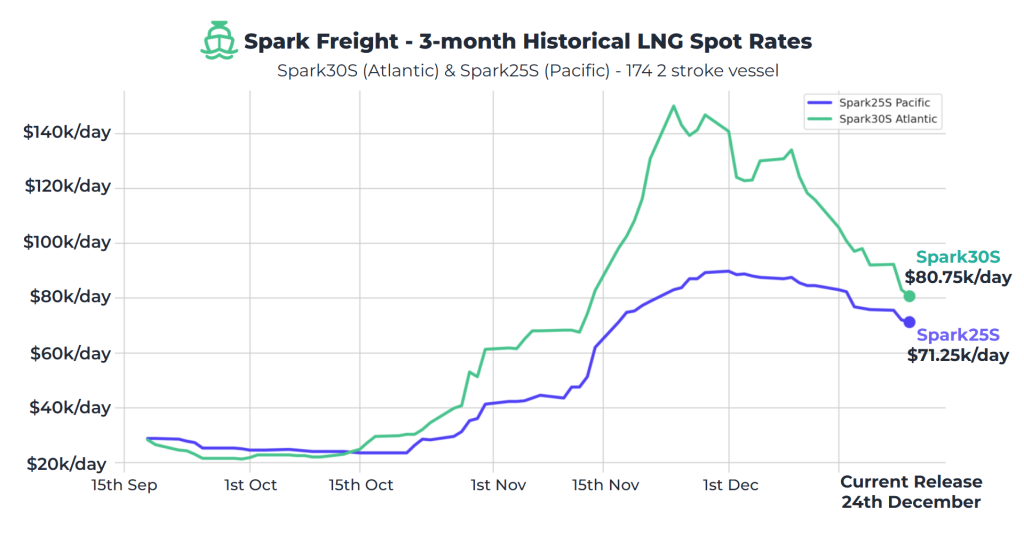

Spark’s data lead, Qasim Afghan, told LNG Prime that Spark30S (Atlantic) LNG freight rates decreased by $11,250 to $80,750 per day.

This data is from Wednesday, as Spark did not publish its prices on Thursday and Friday due to holidays.

“Spark30 (Atlantic) forward freight rates for January 2025 continue to fall this week following further FFA market activity, dropping $25,500 to $25,000 per day,” he said.

Spark25S (Pacific) rates also fell this week, dropping $4,500 to $71,250 per day, Afghan said.

“As Christmas approached, the market was driven less by geopolitics and more by strong LNG volumes, reinforcing shipping as a derived demand,” Fearnley LNG said in its weekly LNG report.

The Oslo-based advisory and brokering firm said that a sharp rise in Atlantic LNG exports in the fourth quarter “caught the market off guard, tightening available LNG shipping capacity.”

“This pushed spot rates into six-figure winter territory, levels not expected in 2025,” it said.

“While most owners won’t be unwrapping a clean term TCP this Christmas, the winter market has reinforced that being short LNG shipping can be costly heading into 2026,” Fearnley LNG said.

“Activity at the yards remains firm, with Hudong-Zhonghua securing a hat-trick of LNG newbuilds for a producer’s fleet renewal requirements. Samsung Heavy Industries is reported to have secured two LNG newbuild orders, supported by longer-term tender business,” Fearnley LNG added.

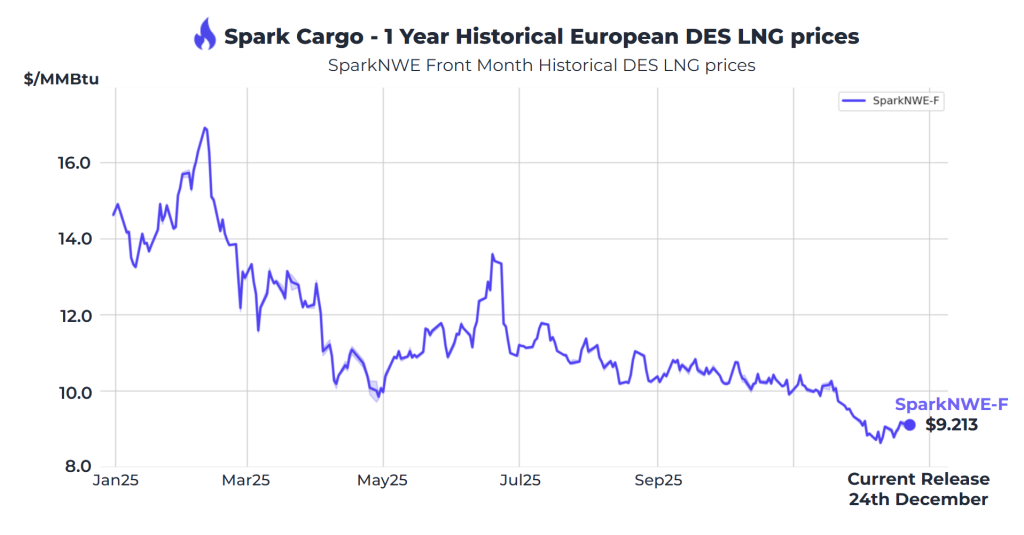

European prices rise

In Europe, the SparkNWE DES LNG increased compared to last week.

“The SparkNWE DES LNG front month price for January increased by $0.204 to $9.213/MMBtu since Thursday, whilst the basis to the TTF is assessed at -$0.485/MMBtu,” Afghan said.

“The drop in Atlantic freight rates has caused the US front-month arb (via COGH) to narrow -$0.220 this week to -$0.160/MMBtu, but is still pointing to Europe,” Afghan said.

“The US front-month arb (via Panama) remains marginally pointing to Europe, assessed at -$0.013/MMBtu. The Nigerian front-month arb (via COGH) has also opened up again and is pointing to Asia, assessed at $0.177/MMBtu,” he said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU dipped from last week and were 65.18 percent full on December 24, 2025.

Gas storages were 68.24 percent full on December 17, 2025, and 74.99 percent full on December 24, 2024.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in February 2025 settled at $9.730/MMBtu on Wednesday.

Last week, JKM for February settled at 9.675/MMBtu on Friday, December 19.

Front-month JKM dropped to 9.590/MMBtu on Monday and it rose to 9.630/MMBtu on Tuesday.

State-run Japan Organization for Metals and Energy Security (Jogmec) said in a report earlier this week that JKM for last week “remained almost unchanged at mid-$9s/MMBtu on December 19 (February delivery) from mid-$9s/MMBtu the previous weekend (January delivery).”

“JKM edged up slightly on December 15 on a rebound following the previous week’s decline, but fell to low-$9s/MMBtu as the contract rolled over to February delivery on December 16 amid ample supply and persistently weak spot demand in Northeast Asia. Thereafter, the price moved within a narrow range between low- and mid-$9s/MMBtu, ending the week at mid-$9s/MMBtu on December 19,” Jogmec said.