This story requires a subscription

This includes a single user license.

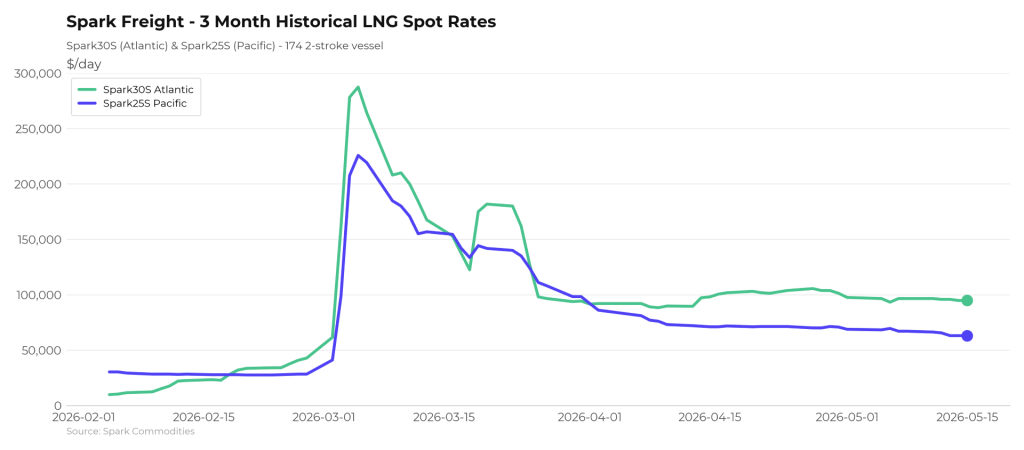

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) rates dropped $1,750 to $94,750 per day this week.

Afghan said Spark25S (Pacific) rates dropped $4,000 to $63,000 per day.

Hormuz LNG transits

“Some significant LNG shipping developments in the Middle East over the past week, as both QELM and ADNOC vessels are reported to have transited the Strait of Hormuz on laden voyages. This marks the first LNG cargoes loaded within the Gulf to exit via the Strait of Hormuz since the conflict began in late February,” Fearnley LNG said in its weekly LNG report on Thursday.

“In the East, sparse May cargoes coupled with ample supply has led to hot competition across the tonnage classes for prompt requirements, while Qalhat volumes continue to provide opportunities to owners that can call there. Requirements are emerging for June but currently these are stacked towards the second half of the month, leaving space for idle time. Requirements out of the US East Coast and especially West Africa are enticing owners to reposition tonnage, offering attractive utilization and a rate premium to Pacific cargoes,” the Oslo-based advisory and brokering firm said.

Fearnley LNG said that “the Atlantic market has proved stubborn, with rates remaining tightly bound in the mid-$90k/d range when accounting for vessel specifications.”

“The requirement list has been uneven, with relatively few cargoes in early June set against an extensive list from mid-June onwards. We may therefore see a little more variability as charterers face more or less competition for individual requirements, but the fundamentals are showing no signs of change in the coming weeks,” Fearnley LNG said.

“Multi-month coverage through Q3/Q4 remains of interest but charterers have eased back on taking on tonnage. The bullish sentiment of the major portfolio players has trickled through the market, and we do see some additional subletters hoping to lock-in utilization, and this may explain the “wait and see” approach among charterers now,” it said.

Continued reduced demand for delivery slots in Northwestern Europe

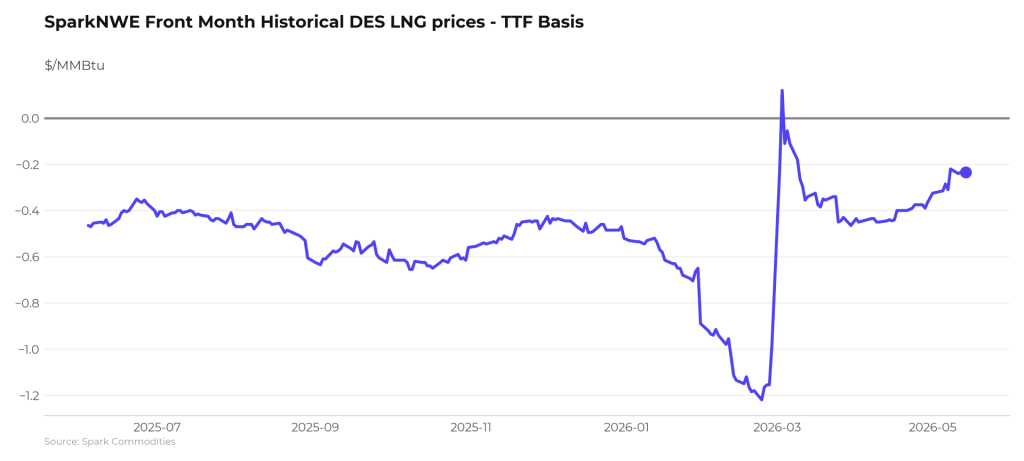

In Europe, the SparkNWE DES LNG rose compared to last week.

“The SparkNWE front-month DES LNG price for June delivery is assessed at TTF-$0.235, indicating continued reduced demand for delivery slots into NW-Europe. The outright NWE DES LNG price is now at $16.078/MMBtu, increasing $1.353 week-on-week and marking the highest front-month DES LNG price since early April,” Afghan said.

“The US prompt (M+1) arb to Asia via COGH remains open and priced at +$0.113/MMBtu – the arb has now been open for two weeks, the longest signal to Asia via COGH since July 2024,” he said.

Afghan added that “the US M+1 arb via Panama remains open and firmly pointing to Asia for an 11th week running, now priced at +$0.861/MMBtu.”

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU rose from last week and were 35.85 percent full on May 14, 2026.

Gas storages were 34.26 percent full on May 7, 2026, and 43.36 percent full on May 14, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in June 2026 settled at $17.065/MMBtu on Thursday.

Last week, JKM for June settled at 16.870/MMBtu on Friday, May 8.

Front-month JKM rose to 16.945/MMBtu on Monday, 16.985/MMBtu on Tuesday, and 17.020/MMBtu on Wednesday.