This story requires a subscription

This includes a single user license.

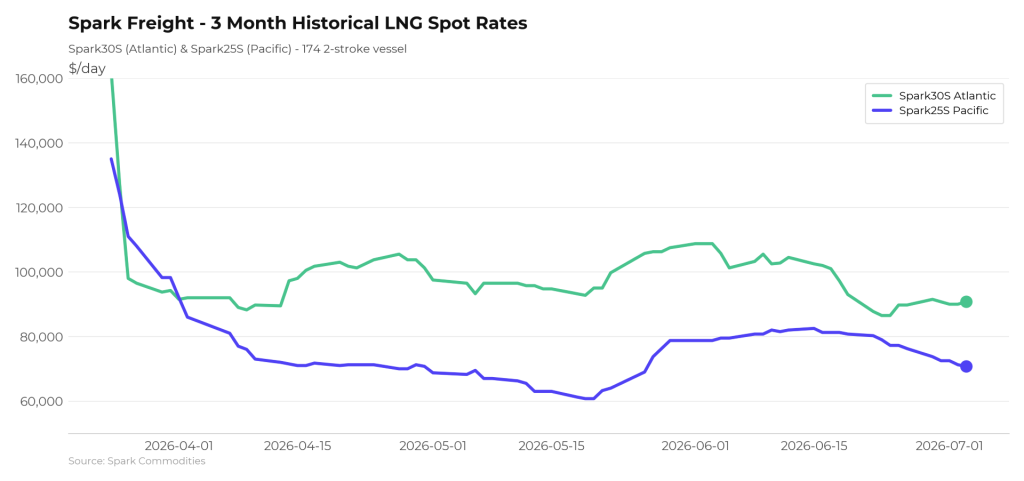

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) rates have remained relatively steady for a second week, increasing $1,000 week-on-week to $90,750 per day.

Afghan said that Spark25S (Pacific) rates have dropped a further $5,500 to $70,750 per day.

Strait of Hormuz

“As many had feared, hopes for resumed safe passage through the Strait of Hormuz in the near future were once again dented as further attacks on commercial shipping were followed by retaliatory strikes on Iran over the weekend,” Fearnley LNG said in its weekly LNG report on Thursday.

“The brief window of free transit enjoyed by LNG carriers last week is back on hiatus and there was an immediate reaction in the LNG market, with pricing into Asia ticking higher and the arbitrage widening,” the Oslo-based advisory and brokering firm said.

“For now, despite continued uncertainty, the summertime lull in the spot market is apparent: availability lists are quite thin but there is also a relative lack of requirements, so there is a slight oversupply of tonnage putting downward pressure on 2-stroke and TFDE rates,” Fearnley LNG noted.

According to Fearnley LNG, this is “more pronounced east of Suez than west, where there is considerable premium, although Atlantic rates dipped below $90,000/day for the first time in months off the back of a rush of QatarEnergy sublets.”

“Looking further ahead, there has been little change for multi‑month periods and rates have remained fairly flat through to 1Q 2027,” Fearnley LNG added.

Increasing demand for delivery slots in Europe

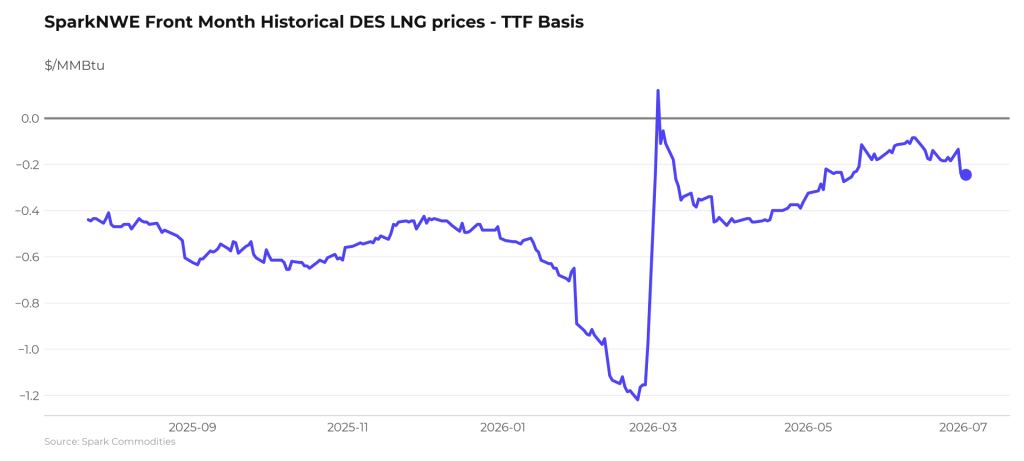

In Europe, the SparkNWE DES LNG rose compared to last week.

“The SparkNWE front-month DES LNG price for August delivery is currently assessed at TTF-$0.245, the lowest front-month basis since mid-May and indicating increasing demand for delivery slots in NW-Europe. The outright NWE DES LNG price is now at $14.516/MMBtu,” Afghan said.

“The SparkUSG-Sabine FOB marker for prompt cargoes is priced at $13.278/MMBtu as of yesterday’s close, increasing $1.189 (+9.8 percent) week-on-week,” he said.

Moreover, Afghan said that “the US prompt (M+1) arb via COGH is currently pointing firmly to Europe at -$0.364/MMBtu, following some region-switching earlier in the week as fluctuating progress in US-Iran peace talks caused volatility in JKM-TTF spreads.”

“The US M+1 arb via Panama remains open and firmly pointing to Asia, now priced at +$0.588/MMBtu,” Afghan said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU rose from the previous week.

Gas storages were 49.22 percent full on July 2, 2026. The storages were 47.43 percent full on June 25, 20266, while the storages were 59.15 percent full on July 2, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in August 2026 settled at $16.080/MMBtu on Thursday.

Last week, JKM for August settled at 15.525/MMBtu on Friday, June 26.

Front-month JKM rose to 15.820/MMBtu on Monday. It rose to 16.050/MMBtu on Tuesday and dropped to 16.025/MMBtu on Wednesday.