This story requires a subscription

This includes a single user license.

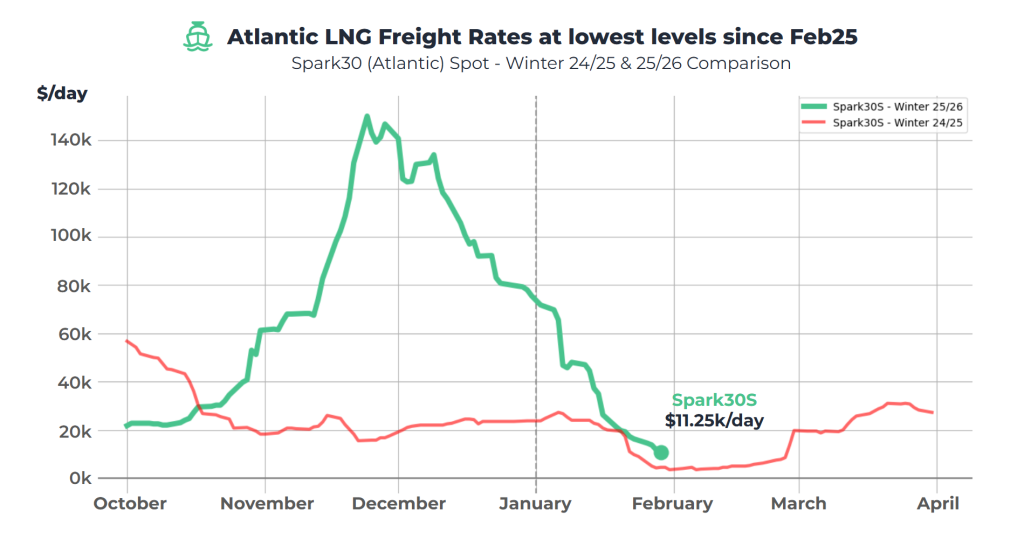

Spark’s data lead, Qasim Afghan, told LNG Prime on Friday that Spark30S (Atlantic) rates dropped for a ninth consecutive week, decreasing $5,000 to $11,250 per day – the lowest levels since February 2025.

Spark25S (Pacific) rates decreased $3,750 to $30,500 per day, he said.

“Spot rates this week continue to soften in the Atlantic, moving quickly from the teens into single-digit territory, with intense competition for cargoes and little indication of a near-term rebound despite some remaining fixing activity,” Fearnley LNG said in its weekly LNG report.

The Oslo-based advisory and brokering firm said that “a short-lived reverse arbitrage could see a limited number of Asian cargoes head toward Europe, though this is not expected to persist.”

“Rates in the Pacific and Middle East remain matterially stroner the in the Atlantic, with East of Suez TFDE vessels securing higher levels than modern 2-stroke tonnage in the Atlantic. This growing regional gap continues to weigh on owners exposed to Atlantic markets,” it said.

Fearnley LNG noted that “a number of 1-3 year fixtures have been concluded at levels pointing to a firmer second half of the year.”

“These deals offer some support for owners facing redeliveries in late 2026,” Fearnley LNG said.

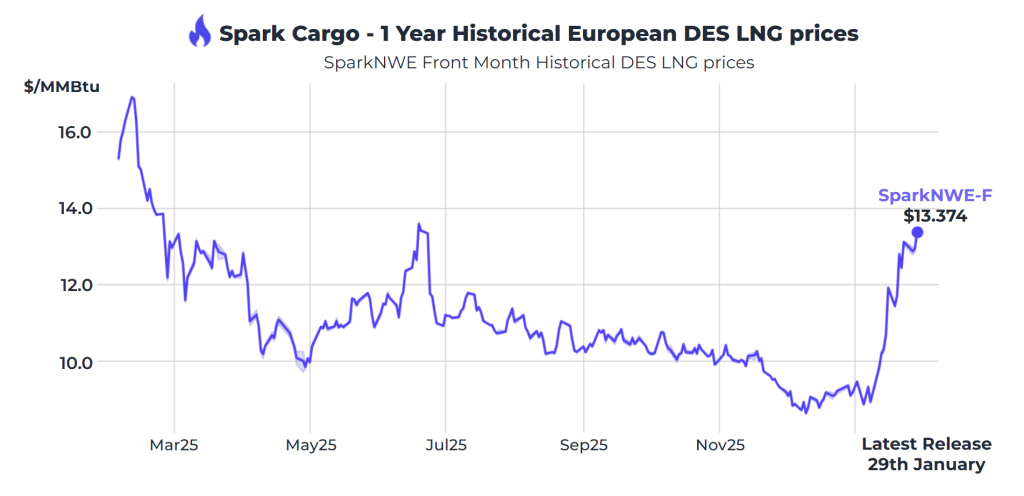

European prices climb

In Europe, the SparkNWE DES LNG increased compared to last week.

“The SparkNWE DES LNG front-month price for February increased $0.93 to $13.374/MMBtu – the highest front-month price since February 2025,” Afghan said.

He said that the basis to the TTF is “assessed at -$0.650/MMBtu and continues to indicate increased demand for delivery slots into NW-Europe.”

“The US front-month arb (via COGH) closed out further this week, currently assessed at -$1.780/MMBtu – the strongest signal to Europe for US prompt cargoes since December 2022 and driven by continuing falls in the JKM-TTF spread as the JKM fails to match the recent TTF rally. Similarly, the Nigerian front-month arb (via COGH) has closed out further and continues to point to Europe, assessed at -$1.435/MMBtu,” Afghan said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU dipped from last week and were 42.90 percent full on January 28, 2026.

Gas storages were 47.63 percent full on January 21, 2026, and 55.05 percent full on January 28, 2025.

JKM

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in February 2025 settled at $11.465/MMBtu on Thursday.

Last week, JKM for February settled at 11.285/MMBtu on Friday, January 23.

Front-month JKM dropped to 11.225/MMBtu on Monday. It rose to 11.350/MMBtu on Tuesday and dropped to 11.290/MMBtu on Wednesday.

Japan’s JOGMEC said in a report earlier this week that the Northeast Asian assessed spot LNG price JKM for last week rose to “low-$11s/MMBtu on January 23 from low-$10s/MMBtu the previous weekend.”

“Spot activity remained limited, but JKM was lifted by strength in the European market, while a cold spell across Northeast Asia supported market sentiment, pushing prices into the $11/MMBtu range,” JOGMEC said.